Nations never experience year-over-year declines in cash in circulation. Sweden (which I wrote about here, here, and here) is one of the rare exceptions. India is another, but this was due to its notorious botched demonetization attempt (which I wrote about here, here, here, and here). But now the UK seems to be joining this small group of outliers.

Why does a nation's cash in circulation generally grow consistently from one year to the next? While economies do experience the odd recession, in general they are always improving. Improving economies coincide with more demand to make transactions, and for this the public needs to have greater amounts of cash on hand. There is a counter-cyclical element to cash holdings. When recessions occur, people often turn to unofficial sectors of the economy to make a living, and this often requires cash. The last explanation for the steady growth in cash outstanding is inflation. Let's assume an inflation rate of 10%. Someone who generally hold $10 worth of purchasing power in their wallet in 2018 will have to hold $11 in 2019 if they want their situation to stay the same. To meet that demand, the central bank has to print more banknotes.

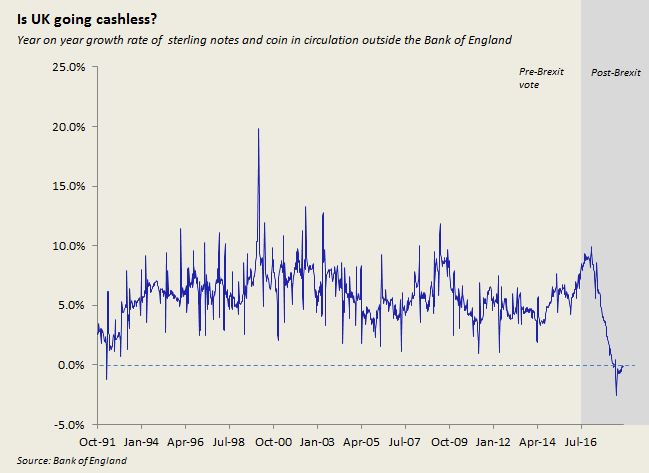

All of this is why the UK's recent flirtation with decashification is so strange. Below is a chart showing the year-to-year change in British paper currency in circulation:

For eight months now, since February 2018, the stock of Bank of England banknotes has been registering below the previous year's count, a phenomenon that Britain has never seen (at least not since the start of the data series I found).

One potential explanation for the recent bout of decashification is increased debit and credit card usage. I am not entirely convinced by this argument. People's transactional habits are notoriously slow to change. When the inevitable card-induced decline in cash does occur, it won't suddenly occur in the space of eight or nine months, but will take place over an extended multi-year period. As in the UK, card usage in Canada is ubiquitous, yet we haven't seen the same sort of effect on the stock of cash. Something unique seems to be occurring in the UK.

The UK has been switching to polymer notes recently, the new £10 being introduced in 2017 and the £5 in 2016. Old paper versions can no longer be spent. The £20 is slated for a switch in 2020. Perhaps this is creating havoc with people's money holding patterns? I suppose it's possible, but here in Canada we went through the whole polymerization process without a hiccup. (See chart here). So I don't see why the UK would experience any sort of discontinuities during its own changeover.

The answer can only have something to do with Brexit. One possibility is that Brexit has reduced immigrant inflows and encouraged outflows, and immigrants are large users of cash. Ipso facto, cash-in-circulation has declined. The problem with this explanation is you'd need really large changes in migrations flows to see that sort of pattern in cash demand, and I am skeptical we're seeing that sort of upheaval.

Another Brexit-based explanation is that Brexit has broken the banknote. British banknotes have suffered a massive credibility shock. All those paper pounds hoarded away under Brits' mattresses, or in criminal vaults, or in foreign pockets, are just not as trustworthy as they were before. So they are being quickly spent or exchanged for other paper, say euros. Eventually these unwanted notes are resurfacing back in the UK where the Bank of England is forced to suck them back up and destroy them.This paints a particularly dour picture. It says that the Bank of England's seigniorage revenues have been permanently damaged, the short-fall having to be made up by the British taxpayer. It makes one worry about potential long-term damages to the Bank's ability to effect an independent monetary policy.

Having had some time to think about this, I think I've got a better story. The changes are indeed Brexit-induced. But the big decline we've seen over the last year isn't a sign of distrust in paper pounds. Rather, it's a reversion to trend. More specifically, the decline in cash-in-circulation so far this year is actually the unwinding of an unusual surge in cash-in-circulation that began in early 2016. Check out the chart below:

Beginning in 2016, as the political competition in the leadup to the Brexit vote intensified, banknotes-in-circulation suddenly started to rise relative to long-term trend line growth (black line). This was the fastest rate at which banknotes in circulation had increased since the 2008 credit crisis. The Bank of England's blog, Bank Underground, commented on the surge in banknote demand back in 2016.

The sudden demand to hold more cash continued through the June 23, 2016 vote into early 2017. I suspect that this was a symptom of an underlying uncertainty shock spreading through the UK economy. Brits were growing increasingly worried about the effects of Brexit. Perhaps they wanted to hold fewer deposits, or have less exposure to assets like stocks and real estate. Cash is a coping mechanism. In uncertain times it one of the few assets that offers the combination of short-term price certainty and the ability to be mobilized in an instant.

This chart from the Bank of England shows that the demand for the the £50 note (pink line) was particularly marked in 2016:

|

| Source: Bank of England |

But by mid to late-2017, Brexit-related uncertainty began to subside, and cash began to be redeposited into the banking system. UK cash usage has now returned to the long-term trendline growth rate. Going forward, I'd expect the year-to-year change in cash outstanding to return to its habitual 5%-ish per year. That is, absent more Brexit-induced panics.

For much of this post, I am indebted to this great round of conversation on Twitter:

That's odd. For most of 2018, there has been no year-over-year growth in the quantity of UK banknotes in circulation. Going back to 1998, this sort of sustained lull in cash demand has never happened. What's going on? Less crime? pic.twitter.com/PXv53oB4E7— JP Koning (@jp_koning) July 18, 2018

I suspect you've missed the salient change.

ReplyDeleteContactless card payments have become mainstream across the UK (but also in Slovakia, the Czech Republic, Hungary and other countries...) at around the same time (coincidental timing).

Even before contactless cards, the UK already had very high penetration of debit card (and credit card) use for retail transactions (over 50% by value). However, people generally only used cards for higher value transactions (> £10) and so people still had to carry cash. Contactless cards have changed that: low value transactions can now be conducted with a tap of the card, without pin entry, and payment processors have changed their fees on retailers to make small electronic transactions an attractive proposition. There's no longer a minimum transaction size to pay by card, paying by card no longer requires pin entry, and payment by card is now an option in more locations than ever before. Quite suddenly, it has become possible to live without cash.

That, surely, is the underlying cause. The UK case is more like Sweden (or Denmark, Norway or Iceland) than anything new or Brexit related. Other European countries (such as Czechia or Slovakia) are moving rapidly in the same direction.

I think this is right.

Delete"Quite suddenly, it has become possible to live without cash."

DeleteFor sure. But Canada has also gone through the exact same experience, and we haven't seen a downturn in cash outstanding. Australia dominates the list of contactless countries, but banknotes in circulation continues to grow. There is something unique going on in UK, and it isn't contactless. It's got to be Brexit.

You mention Iceland, by the way. Huge growth in cash outstanding, even though contactless card payments are very popular:

https://www.bullionstar.com/blogs/bullionstar/the-future-of-cash-iceland-vs-sweden/

Regarding cash issuance... Iceland is not a typical case - tourists visiting each year outnumber inhabitants by a multiple of around 7, and many tourists leave with a bit of Icelandic cash, never to return again (withdrawn from effective circulation forever). Iceland's "cash outstanding" (in reality: cash created, taken away by foreigners and lost forever) will continue rapid growth for as long as Icelandic cash is still a thing that tourists pick up.

DeleteThe comparison to make between the UK and Scandinavian countries is in the high prevalence of cashless payments (universal adoption by retailers; high popularity among the population). In the UK, 76% of all transactions (by number of transactions) and around 90% of all transaction value is paid by card (by latest BRC numbers). That's not yet at Scandinavian proportions - we're still a decade or so behind (but catch-up might not take a decade). It doesn't look like either Australia or Canada have reached that depth of penetration yet. It's quite different from the United States, where transaction fees are generally far higher and many retailers refuse to adopt; or Germany where users don't trust electronic payments operators/ government with their transaction data; or Italy where cash-in-hand is essential for petty tax avoidance; or Central Europe where a large portion of the population is unbanked and doesn't have access to the necessary cards.

Perhaps the key to declining cash outstanding really is Brexit: afraid of Brexit pensioners are emptying their mattresses and investing in currency-hedged ETFs; afraid of Brexit, cocaine dealers are switching to euros and Swiss francs? Or maybe, just maybe, demand for cash is falling as people feel they can comfortably live for months (or years) at a time without ever touching a banknote or coin?

When I was writing the blog post about Iceland I overlaid Iceland's monthly cash-in-circulation on top of its monthly tourism visits. Cash outstanding actually peaks in December, when there are no tourists... not in summer which is peak tourist season. So I don't put much stock in the idea that tourists to Iceland are driving its growth in cash.

Delete"Perhaps the key to declining cash outstanding really is Brexit: afraid of Brexit pensioners are emptying their mattresses and investing in currency-hedged ETFs; afraid of Brexit, cocaine dealers are switching to euros and Swiss francs?"

I hope you don't think that was my theory. My theory was that anxious Brits were holding more cash in 2016 and early 2017 due to concerns over Brexit, and now they aren't so anxious and are returning it. Thus the year-over-year decline.

Let's revisit this in 12 months. If I'm right, growth in cash-in-circulation will have returned to it's previous range. If you're right, it should keep falling.

If it's Brexit why did it also happen in 1991?

ReplyDeleteI must confess that I did dig around to find out what happened in March 91-to-March 92 but had no success. Negative growth was just fleeting, though, lasting just two weeks.

DeleteThat's interesting - a 1992 blip supports the notion that speculative currency holding (and hence events such as Brexit) might actually matter.

DeleteNotably, the UK crashed out of the ESRM in September 1992 (black Wednesday, massive devaluation). The large current account deficit, and the BoE's funding shortage were evidently unsustainable. Perhaps some speculator agents (e.g. banks, which hold some reserve of cash as banknotes) made a concerted effort to reduce their exposure to a likely sterling devaluation?

If it has happened before, it could feasibly have happened again (as Brexit justifies a tangible fear of sterling depreciation). But then: where are these large stocks of banknotes held, and why would anyone be (A) so unsophisticated as to hoard notes but (B) sensitive enough to control their exposure to FX movements?

I imagine the difference is due to what suppliers are willing to accept rather than demanders are able/wanting to pay in.

ReplyDeleteCashless existed before cash, ergo must people have access to it all the time unless it is for something out of their normal routine.

for them to change their habits instantly indicates a change in what most suppliers are willing to accept.

did anything happen?

it seems unlikely a lot of suppliers who could process cash previously would suddenly turn down cash, cashless they do turn down for low amounts.

the only people who might be willing to accept cashless who previously didnt would be the 'cash-in-hand' guys.

did 'cash-in-hand' suddenly go out of fashion?

i think the gig economy mob might have something to do with it.

plus supermarket 'people free' checkouts. using cash is a pain

ReplyDeleteI wonder if the amount stored in ATMs has fallen. We used to have three machines in our village, sometimes with queues. Now we have one and no queue. With 700+ ATM robberies per annum, machine operators may be reducing amount kept in the machines. Closed bank branches also hold no cash!

ReplyDelete