The outbreak of Covid-19 has caused a global increase in the amount of cash in the economy. I think I've got a pretty neat explanation for why.

But before I tell you what it is, let me show what the cash build-up looks like. Here's what has happened to banknotes in circulation in Canada so far in 2020:

The quantity of Canadian banknotes in circulation keeps rising. 19 consecutive weeks without a decline. Unprecedented.— John Paul Koning (@jp_koning) July 27, 2020

Any theories? I have one—will write a blog post soon.

(In a counterfactual world without COVID, we'd be at C$94 billion notes outstanding, not $101 billion.) pic.twitter.com/rIWyUqEPnx

Meanwhile, here is the US:

U.S. banknotes in circulation, by year.— John Paul Koning (@jp_koning) July 7, 2020

Usually so predictable, but not in 2020... pic.twitter.com/sdkBvorhtS

And here is the UK:

Each chart shows an unusual increase in banknotes in the economy starting in March or April, when the pandemic first hit western countries. These cash bulges show no signs of shrinking. And they are quite big. In the case of the U.S., I'd estimate that there are $150 billion extra paper dollars in circulation thanks to the virus.There's been a big jump in UK banknotes in circulation since the COVID outbreak started. Oddly, this is happening as ATM cash withdrawals have collapsed by as much as 60%. pic.twitter.com/w3taggoaib— John Paul Koning (@jp_koning) July 31, 2020

I recently came up with a surprising explanation for why this is happening. But before we get to it, we need to review what determines the amount of cash held in the economy. Here's an analogy. Think about how the water level in a reservoir might rise. There are two ways this can happen. More water can run into the reservoir, or less water can flow out. (Conversely, the water level can fall when either less water enters, or more is withdrawn.)

The same principle applies to the amount of cash held in the economy. If more people are taking cash out from ATMs and banks then the amount of cash in the economy will grow. But the amount of banknotes in the economy can also grow without a rise in withdrawals. That can happen when the public (i.e. individuals & businesses) returns less of the stuff than before to ATMs and banks. So more of it stays floating around in the economy.

Now, I must confess that in previous blog posts and tweets I had assumed that the big increase in cash-in-circulation during the pandemic was due to an increase in withdrawals. People were worried about the virus, I thought, so they wanted to take more banknotes out of their bank accounts and hold it under their mattresses. "Cash restocking makes sense in an emergency like the one we are living through," I wrote back in April. And here: "The coronavirus reminds us of the fragility in our infrastructure. And so we rebuild some of our banknote balances."

But now I think that I was wrong. The big increase in cash-in-circulation is not due to an increase in withdrawals of cash. Sure, some people are taking out a few more $50s or $100s to hold under their mattress. But with the virus shutting down the economy, most of us are making less purchases than before. The few transactions that we continue to make tend to be digital, say like buying from Amazon with a card. The net effect is that since March we have been withdrawing far less cash than normal.

If so, then why has the level of cash in the economy jumped? The only explanation is that there is much less cash being returned to banks and ATMs. Businesses and individuals simply aren't redepositing their banknotes. There's some sort of clog or blockade that is gumming up the system and preventing a regular flow of returns. I'll try and explain the precise nature of this clog, but first lets look at some data that confirms that returns of cash have dried up.

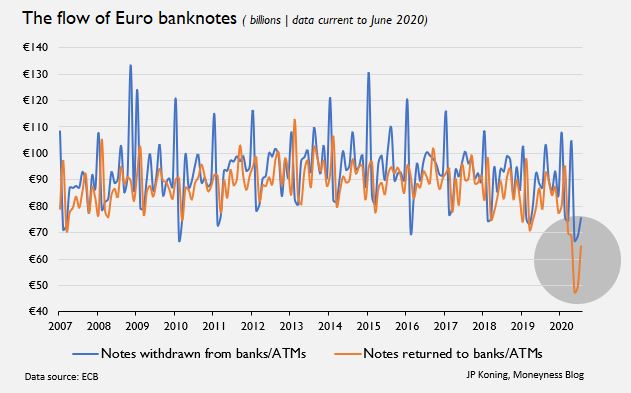

The European Central Bank (ECB) is unique. Most central banks only provide public data on the net amount of cash that is in circulation. But the ECB goes the extra step and offers data on both the flow of banknotes being issued into the economy and the flow being withdrawn from the economy. And so we can actually see which half of the equation is responsible for the big jump in cash: more withdrawals or less returns.

As you can see, Europe has seen a large and anomalous jump in cash-in-circulation in 2020, just like Canada, the US, and UK. I've charted this below:

Now let's see what the ECB's disaggregated data has to say:

In general, withdrawals of euro banknotes (the blue line) has exceeded returns (the orange line) from 2007 to 2020. That's why the amount of cash in the European economy has generally increased over time. During the 2008 credit crisis, there was a big jump in withdrawals, no doubt to worries about the safety of the banking system. But during the pandemic, cash withdrawals (blue line) have actually fallen, not increased. In fact, the level of withdrawals is at its lowest point in over a decade!

Returns of cash (orange line) have plunged by even more than withdrawals. They are at their lowest level ever!

So what does this mean? Thanks to the pandemic, European individuals & businesses have become less interested in taking cash out of the bank. But they are even less interested in returning cash to the bank. It is this outsized collapse in returns, the orange line, that is causing the big build-up in euro banknotes in circulation.

For those who like analogies, let's revisit our reservoir imagery for a moment. The amount of water (i.e. cash) flowing into the reservoir (i.e. the economy) has slowed to a trickle. Normally this trickle would lead to a fall in the water level. But because even fewer people are removing water (i.e. doing cash returns) from the reservoir, the incoming trickle is sufficient to push the water level higher.

I think there's a good chance that what is happening in Europe is happening in the U.S., Canada, and U.K. too. Thanks to the virus, no one is redepositing their banknotes. But I'd have to see the data to be sure.

Now we can finally get to my theory for what is clogging up the system. The peculiar feature we need to explain is people are so much less willing (or able) to return their notes during the pandemic than they are willing to withdraw them. Or put differently, why did the orange line fall so much more dramatically than the blue line did? It suggests some sort of asymmetry in people's usage of cash. My theory is that this asymmetry can be found in the nature of the black market, illegal drug markets, the mob, the underground economy, etc.

The specific asymmetry is this: it is quite easy for a drug buyer to withdraw $200 from an ATM to buy heroin or cocaine. Banks don't surveil people who are taking out cash. But it is far more complicated for a drug seller to redeposit that $200. Redeposits are surveiled. To get banknotes back into the system a crook has to launder them, say be sneakily mixing the drug money with legitimate cash earned by

Let's work through how this specific asymmetry has collided with the pandemic. It's unlikely that drug users have stopped buying drugs during the pandemic. (Maybe people are buying even more drugs? Thanks to shut downs, there's not much to do!) So the flow of cash from a drug users' ATMs to a drug dealers' pockets has not slowed at all during the pandemic.

But the network of restaurants and other businesses that drug dealers rely on to launder their funds have all shut down thanks to virus fears and lockdowns. These closures would have put drug dealers, crooks, the mob, etc. in a tough position. Throughout the pandemic they have been accumulating ever more cash from drug using customers, with no place to offload it.

So to sum up, the big increase in cash in the economies of Canada, Europe, US, and the UK is probably being driven by an unwanted accumulation of cash by crooks. Their regular money laundering arrangements aren't functioning.

I don't have any personal experience with being a criminal. But it's fun to speculate about what their lives have been like during the pandemic. The Tony Sopranos, Walter Whites, and Stringer Bells of the world are currently scrambling around for safe places to store their ever burgeoning stores of physical cash. In their houses, at a warehouse storage unit, or at a bank.

And since they can't convert their cash hoards into spendable money in a bank account, I'd imagine these crooks are having problems paying legitimate bills like mortgage payments and the cost of sending their kids to posh schools. With criminal enterprise handling so much extra cash, I'd also imagine that law enforcement agencies are seizing record amounts of cash via civil forfeiture. We could also be seeing a big jump in gang warfare as competing drug outfits raid each other for cash. To recover all of these extra costs of doing business, criminals are probably jacking up drug prices. Yep, I'd imagine it's not an easy time to be a criminal.

As the pandemic subsides and restaurants and other confederate businesses start to open, criminals will be able to restart their money laundering operations. But they won't be able to return their entire accumulated hoard at once. If they were to do so, the cash receipts of the businesses they are using for laundering would stick out, potentially drawing the attention of the tax authority and law enforcement. No, they'll have to slowly reintroduce their dirty money.

Which means the big global jump in banknotes that I illustrated in my first set of charts will take much longer to be worked off than it was accumulated.

PS: I wonder if we can get some other good insights from the data, specifically about the size of the underground economy. Looking at my topmost chart, I'd estimate that the amount of cash in the Canadian economy is about $6 billion higher than it would otherwise be. Let's say that this bulge is entirely due to criminals being unable to launder their drug proceeds. We know Canada has 32 million adults. So Canadians have spent $6 billion on illegal drugs since the pandemic began, or around $200 per adult. That's about $12 billion a year. Seems reasonable, no? (Yes, I am making a load of assumptions here.)

I’ll think more about your overall thesis, but there may be an additional piece that could complement your explanation.

ReplyDeleteUntil very recently (a week or two ago), most full service Canadian bank branches have been closed since March. ATM access remained open in many cases, but not in-branch counter service. Select branches remained open for full service – but very few (if my own well banked suburban area is an indicator).

Perhaps that’s been an additional constraint on normal behavior in terms of the return flow of bank notes.

Hi JKH,

DeleteI wasn't aware of that, thanks. That could have had some impact on reducing returns. I suppose it might have also had an equal impact on reducing withdrawals, too?

I think it’s possible that smaller businesses that stayed open or re-opened early (e.g. convenience stores) may have reduced the frequency with which they take their surplus cash into the branch for deposit. That might correlate with the fact that so many branches were closed, and that businesses with cash to deposit were inconvenienced as a result.

DeleteI'm not familiar with procedures where they might use bank drop boxes instead of the branch counter - but I'm guessing such facilities may also have been sealed off, given the lack of branch personnel to service them. Anyway, I'm thinking many of these businesses prefer to use the branch counter to deposit their cash in any event, where they can confirm bookkeeping records etc. with some immediacy.

So that’s a possible asymmetry between cash outflow from ATMs / branches and cash returning to branches. Just my speculation. Perhaps one of your readers has greater knowledge of such small business cash management practices.

Regarding branch closure – if you’d posted a couple of week ago, I would have suggested googling bank branches for any of the Canadian banks, and you would have seen a Google Map displaying all branches and their open/closure status for any chosen geographic area. I’d guess at least 80 per cent of branches were closed for most of the past 3 months prior to that point. Unfortunately, or fortunately, it appears most have re-opened in staged fashion, so that effect won’t be apparent now.

So - with respect to access - perhaps an asymmetry between retail customers withdrawing nearly as frequently using ATMs, versus retail business redepositing less frequently through less available full branch banking

DeleteYou could be right, JKH. I don't know enough about the intricacies of small business cash management. Do most drop off their daily cash takings in the exterior night deposit box or do they prefer to go inside? If inside, then you've got yourself an asymmetry. But if the exterior deposit box, I think an asymmetry is less likely.

DeleteNice theory — I agree that the reason might be because of less redeposits.

ReplyDeleteHowever, can’t it be as simple as bank branches being closed or people not wanting to go to the bank to deposit their cash because of the virus?

It's possible, Vinny.

DeleteBut if the public doesn't want to go to the bank to deposit cash because of virus concerns, wouldn't they be just as hesitant to go to the bank to withdraw cash? We need a theory for why the public has reduced its rate of redepositing by more than it has reduced its rate of withdrawing.

One should consider the utilization of debit isnt universal. For some, you have to withdraw cash to live, but you dont have to necessarily deposit it again after that. I would argue that a lot of people are seeing an unnecessary trip to a bank as a risk but still see a visit to a bank to get money as necessary.

DeleteThanks for the reply, JP.

DeleteYes, I agree with unknown commenter that withdrawing is necessary, but depositing is not so necessary. Just anecdotally, I see this pattern of behavior among my immediate family members. But more importantly, I think — what’s the point of redepositing if interest rates are very low and asset yields are also low. The risk-reward might not seem so good.

Which isnt to say that the underground element isnt a factor. It very well could be, it’s just hard to measure. Thanks!

Interesting theory. Some restaurants and retailers in Europe are only accepting card payments due to concerns that the virus can be transmitted through banknotes and coins. This could also explain the large decline in notes returned to banks.

ReplyDeleteThe criminal story makes sense on its own, but I wonder if a simpler story suffices. I have a few thoughts - (1) asymmetric effect of not wanting to leave house, (2) bank services, and (3) hidden asset hoarding before bankruptcy.

ReplyDeleteMost people don't want to go outside, but some activities are especially NOT WORTH IT. Physically handling cash is another trip that we have to make - both in order to pick up cash and in order to deposit cash. If I need cash, I will accept the incremental risk to go out and acquire cash. Presumably I value what I receive more than the cash I handed over. However, if I receive cash I am not nearly so willing to accept the incremental risk and deposit it in person. Converting liquid assets into a slightly more convenient form is not worth the incremental risk.

Second, cash doesn't tend to circulate evenly through the economy. There are many more buyers than there are sellers, so that sellers (businesses) are generally cash recipients and buyers are cash providers. However, retail banking from an ATM is convenient for the many people who only need a few hundred dollars. The ATM is impractical for the businesses that need to deposit thousands of dollars, and so actually need the bank branch personnel. With Covid-19 affecting the productivity of bank branches (hours, social distancing reducing bandwidth, etc.) it is more costly for the businesses to redeposit cash so they are more likely to accumulate a larger balance than they would have in the past.

Third, for businesses that are likely to go bankrupt soon it is probably not a bad idea to literally has cash squirreled away. They are "looting" their cash flow so they can reduce their losses when the business closes and the lenders try to recoup their losses.

Some good points.

Delete"The ATM is impractical for the businesses that need to deposit thousands of dollars, and so actually need the bank branch personnel."

Large businesses don't return cash by going to the bank. They use cash-in-transit companies like Brinks. I can't imagine this would have been impaired. But yes, small businesses do bring their cash taking to the bank.

As I was discussing with JKH above, are these businesses reliant on going into a bank and dealing with a teller? Or do they tend to drop it in an exterior drop box? If the drop box, I can't imagine there being any reason for a business to accumulate cash.

You may appreciate the estimates of the shadow economy by Medina and Schneider: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3502028. They estimate that the shadow (or informal, or cash) economy was 12% of GDP in Canada in 2017. (That is a relatively low value compared to other countries, but it is higher than the United States or UK). Note that the authors use various methods to exclude criminal activities from their estimates. What is left are activities that are primarily conducted in cash, and may not be reported for regulatory or tax reasons. That is a slightly less nefarious angle.

ReplyDeleteNote that the BIS finds a negative relationship between the use of digital payments and the estimated size of the informal economy: https://www.bis.org/publ/arpdf/ar2020e3.htm.

DeleteThanks for the links, anon. I'll check them out.

DeleteNice enough idea, but I simply just have to agree with JKH, Vinny and at least one of the Anons above.

ReplyDeleteOur experience in the UK, mirrors JKH's. The banks simply shut the counter service at branches (or those branches that are still left, anyway). Additionally, in the UK, the overnight deposit boxes have also been steadily removed over the years, even if the branch itself has not (yet) been closed.

Again, businesses became averse to handling cash almost before the lockdown began, urging card payments where possible.

Further, our experience is that where we've helped out with odd bits of shopping for neighbours, friends and relatives, they have paid us in cash. Which we've simply not been able to get rid of, up until about mid-June or so.

As an aside, I'm fairly certain that the BoE does maintain a data series of notes and coins held at financial institutions.

This increase in banknotes did not happen in Sweden, see https://www.riksbank.se/en-gb/statistics/statistics-on-payments-banknotes-and-coins/notes-and-coins/. Bank notes in circualtion peaked in 2009, then declined by 50% until 2017, and has been increasing very slowly since then.

DeleteTHe kind of person-to-person payments you mention, in Sweden they are done using Swish (like Venmo, except the money goes bank account to bank account).

Swish launched in 2012, so it is not solely responsible for the decline, but it might explain why the increase in bank notes did not happen here.

Your theory of a money-laundering bottleneck as a major factor seems plausible enough to me, but I have to take issue with your stereotyping of drug dealers.

ReplyDeleteI was a major player in the Montreal marijuana market in the late 90s and early Oughts, with revenues in the low millions/year. The culture in the industry and the character of the players in it were very different from what's portrayed in the mainstream media and fiction.

Some of the factors that determined this culture were the following:

1) The severity of legal penalties * the probability of getting caught.

Sub-markets with higher penalties and more eager enforcement by authorities attracted individuals with higher risk tolerances and weaker morals. As penalties tend to be roughly proportional to the potential harm done by the drug in question, harder drugs like crack and heroin were sold by comparatively more callous individuals with higher time preference/lower understanding of the reality of the future and the costs of violence. But softer substances like marijuana attracted little attention from law enforcement and did no harm to customers. Participants in these markets were generally upstanding people.

2) The social cost of the profession.

Then, as now, there was a serious social stigma associated with selling drugs that could kill customers, or ruin their lives. Marijuana had become generally understood to be benign, and sellers/growers suffered no loss of social status for their involvement; it was a more or less respectable profession.

3) The ease of production.

I've never yet heard of anyone in Quebec cultivating opium poppies or coca plants, but everyone and his uncle had marijuana grow ops even then. Many of my suppliers were retired Boomer couples with a side hustle to supplement their pensions.

4) The absence of third-party dispute adjudication.

With no courts or arbitrators to decide on conflicts, or breaches of contract, reputation was of paramount importance. Loose communication networks ensured that anyone who tried to pull a fast one soon found no one returning their calls. Cash on the barrelhead was the rule, and the use of credit was minimized. These factors continuously weeded out the irresponsible, shady and undercapitalized players. Over time, the industry became dominated by people who well understood the "discipline of continued dealings."

All of these factors, together with the larger size of the pot market, increased the pool of high-quality competitors, and competition is the health of any market. It led not only to drastic reductions in the use of violence (I never saw any in my ~7 years of involvement), but also to significant improvements in price, quality and service for retail customers. A gram of retail hashish cost $10 in 1980, and a gram of pot cost the same in 2003. It's even less now. This means that the real price has been declining by _at least_ the rate of inflation across the entire period.

What's striking about this whole business is that all the theoretical benefits of the free market have manifested even in the absence of "helpful" state regulation, and despite all the friction of illegality. Market sceptics should take note.

Hi anon,

DeleteThanks for chiming in.

"...but I have to take issue with your stereotyping of drug dealers."

Fair enough. Unfortunately my only anecdotes come from shows like the Sopranos, The Wire, Breaking Bad, and a few others. I enjoyed your comment. It provides a lot of useful details that I didn't know about. It sure would be interesting to hear some anecdotes about how you laundered your funds.

I like your argument. I wonder if the lack of access to the normal money laundering outlets might also have contributed to the strength of cryptocurrencies through the pandemic?

ReplyDeleteGood question. It's a possibility I've considered. Unfortunately I have no way to prove it. In general, I suspect that as cash payments becomes less common, criminals will be forced to develop substitute laundering routes, of which cryptocurrencies will be key.

Delete