To soften the blow of the COVID-19 pandemic, the Bank of Canada is running what it sees as an expansionary, or loose, monetary policy. I think an expansionary policy makes a lot of sense.

The problem is this. The Bank of Canada has several tools it can use to loosen. Some are better than others. But it has stopped trying to use its best tool.

What is its best tool? Well, there are three ways that the Bank of Canada can loosen monetary policy.

Say interest rates are at 4%. Stephen Poloz, the Governor of the Bank of Canada, can either...

1) Cut the interest rate, say to 3.75%

2) Keep rates at 4% but do $20 billion or so in quantitative easing. This is just a fancy term for buying up assets like government bonds.

3) Keep rates at 4%, but promise to maintain them at 4% for extra-long. This is known as forward guidance.

Let me explain the third, forward guidance, because it's complicated. Basically, Poloz says that he will keep the Bank of Canada's interest rate at 4%, but promises to maintain it at that level for longer than would otherwise be warranted. The intuition here is that by committing to keep interest rates extra loose in the future, he can loosen monetary policy now.

I like to think about forward guidance in terms of raising children. Say that I want to modify the behaviour of my three-year old kid. To do so I might reward him with an M&M. Unfortunately I don't have any M&Ms on me. So I promise to give him an extra M&M after the next trip to the grocery store. Hopefully this "guidance" about future M&Ms is enough to get him to do what I want, now.

So which of these three is the Bank of Canada's best tool?

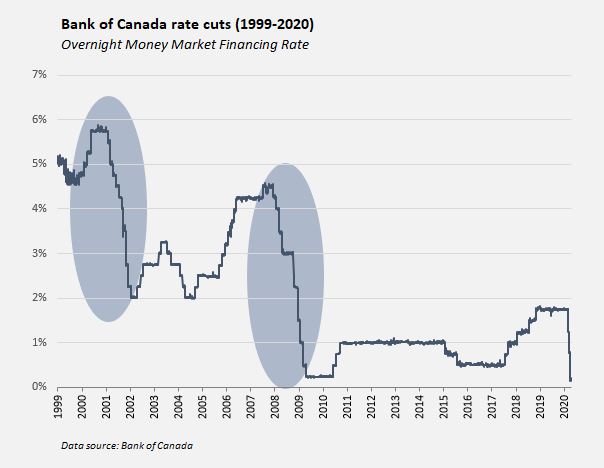

The Bank of Canada's actual behaviour over the last few decades hints at what tool it considers to be the most useful. In 99% of the cases, it has chosen to loosen policy by dropping interest rates, not by embarking on quantitative easing or forward guidance. It usually does so in 0.25% increments, but when the economic shock is large, it'll resort to large interest rate cuts. For instance, after 9/11 it chose a 0.5% reduction.

What about the current episode? The Bank of Canada describes the coronavirus fallout as "unprecedented". In its recent monthly monetary policy report, the Bank says that the severity of the current shocks has inspired it to roll out a "bold policy response."

But if the Bank's policy response is so bold, why has it stopped using its favorite monetary policy tool? Having reduced interest rates to 0.25%, the Bank of Canada says it won't drop them anymore. According to Poloz, interest rates now sit at Canada's "effective lower bound." The implication of his phrasing is that not even a force of nature could move rates below 0.25%.

But that's simply not true. The Bank of Canada's favorite tool isn't stuck at a lower bound. It would be pretty easy to implement another four interest rate cuts. This would take the Bank of Canada's interest rate from 0.25% to 0%, then to -0.25%, -0.5%, and -0.75%.

Don't take it from me. In this 2015 Bank of Canada working paper, researchers Jonathan Witmer and Jing Yang estimate that the Canadian effective lower bound is likely between -0.25% and -0.75%, with a midpoint estimate of -0.5%. Canada would hardly be unique if it went into negative interest rate territory. Other countries have tried negative rates, including Switzerland, Sweden, Denmark, and the European Union.

There's a good chance we'll need it. If we look at previous recessions, we generally got about 4% in interest rate cuts. During the 2001 tech meltdown, the Bank cut from 5.75% to 2%. In 2008 it went from 4.5% to 0.25%. But in our current recession, we've gone from 1.75% to 0.25%. So all the Bank of Canada wants to give us in 2020 is a paltry 1.5%. What a gyp.

What about the Bank's other options for easing? In the last week of March, the Bank of Canada announced a quantitative easing program of $5 billion per week. But by the Bank of Canada's own demonstrated preferences, quantitative easing can't be a great tool—in previous easing periods, the Bank of Canada didn't bother with it.

The problem is that quantitative easing doesn't do much. It sounds big and hefty. But in actuality, big purchases of government bonds are a bit like trying to move a jet plane with a fan. They're certainly no substitute for another rate cut.

As for forward guidance, the Bank of Canada hasn't announced it yet. But any parent knows that a promise of future M&Ms just isn't good as M&Ms in the present. Kids are skeptical of promises, and for good reason.

Stephen Poloz has described negative rates as "not sensible". Here's what is not sensible. We are currently in the midst of the fastest slowdowns in Canadian history, and the Bank of Canada staidly refuses to even consider the possibility of using its favorite and most effective instrument; interest rate cuts. I'm not saying that another rate cut is warranted. But Poloz should at least unshackle his best tool.

P.S. I've been down this rabbit-hole before.

In that post, I speculate why Canadian policy makers seem loath to consider further rate cuts into negative territory.

Look, Canadian regulators have always had a close working relationship with the big banks. This certainly had its benefits. But here we are seeing one of its drawbacks. Canada's big banks are conservative and afraid of change. They probably don't want to incur the frictional costs associated with transitioning to a negative rate environment. And they have probably voiced their concerns to the Bank of Canada. And so the Bank is supporting the banks by declaring the effective lower bound to be at 0.25%. This decision comes at the expense of all Canadian citizens. We all benefit from the ongoing usage of the Bank of Canada's strongest tool: variations in the rate of interest. QE and forward guidance are poor fill-ins.

P.P.S. I just stumbled on Luke Kawa's series of tweets from a few weeks back on the topic of the Bank of Canada's effective lower bound. He captures my thoughts too.

Imagine if the Fed came out of nowhere and dropped a bombshell that it lost 75 basis points of policy space without even acknowledging it.— Luke Kawa (@LJKawa) March 27, 2020

Why do you think, "quantitative easing doesn't do much"? In your language: doesn't increasing the supply of base money lower its convenience yield?

ReplyDeleteBJH, you're right. Given the language I've used in the past, increasing the supply of base money does lower the convenience yield.

DeleteIn the Canadian system, the convenience yield on settlement balances is measured by the distance between the overnight rate and the deposit rate (in the U.S., this is interest-on-reserves). That's generally about 0.25%. It doesn't take too much quantitative easing to reduce the convenience yield to 0. When that happens, the overnight rate trades at the Bank of Canada's deposit rate. At that point, additional QE can no longer have any effect on the convenience yield.

So that's why I say QE doesn't do much. Once the gap between those two rates is at zero, then only subsequent rate cuts will work.

More here: https://jpkoning.blogspot.com/2013/11/rates-or-quantitites-or-both.html

QE does not just increase the quantity of base money, it also increases the amount of commercial bank deposits. The CB creates base money in the CB account of the commercial bank where the bond investor has an account. The commercial bank creates deposits in the account of the investor.

DeleteThis matters because, it is specifically one of the differences between QE and regular CB intervention in the FED funds market. It removes the "crowding out" effect of the abundance of government bonds, and increases the price of commercial bonds and decreases the cost of corporate funding, and even makes investors pro-active in encouraging entrepreneurs in generating new interest generating enterprises.

"This matters because, it is specifically one of the differences between QE and regular CB intervention in the FED funds market. It removes the "crowding out" effect of...makes investors pro-active in encouraging entrepreneurs in generating new interest generating enterprises."

DeleteSorry Dinero, I don't get that second paragraph.

Thanks JP. At the very least, doesn't *permanent* QE today lower *future* convenience yields, for any time in the future when that spread is positive?

ReplyDeleteYes, that's right. It lowers future convenience yields.

DeleteMind you, since the future spread is never going to be more than 0.25%, that means QE can't get a huge amount of traction.

It could be lobbying by large Canadian banks who want to protect their net interest margins. But it could a technocratic assessment that the costs outweigh the benefits. Negative rates hurt bank profits and so can reduce future credit creation and make banks take actions to preserve margins. For instance by hiking lending rates. Perhaps worries about bank earnings/profitability are making the BoC err on the side of caution. There is also evidence that pass through on sub-zero cuts to lending rates is limited (or even negative) - but to be fair these effects only start to kick in way below zero.

ReplyDeleteI also wonder why you think QE is ineffective. What about the role that QE can play in strengthening forward guidance and the impact it has through other channels such as portfolio rebalancing (I think you have discussed this by referring to the 'hot potato' effect in the past)

To add to my previous comment, this was the explicit rationale offered by the members of the MPC in the UK for their decision not to set interest rates lower than 0.5% (https://www.parliament.uk/documents/commons-committees/treasury/130516-Charles-Bean-to-the-Chair-Negative-Interest-Rates.pdf) though this logic applies equally, if not more so, to rates below 0%. On the flipside, banks have demonstrated in other countries, particularly the Eurozone, that they can adjust to lower rates and remain profitable, so perhaps this worry is misplaced.

DeleteHi James,

DeleteI agree that there are some differences between carrying out rate cuts in positive rate territory and negative rate territory. Banks profit on the spread between deposit and lending rates. There may be some stickiness at 0% such that banks do not immediately pass off negative rates to their retail clientele. This may reduce their margins.

But I'll just repeat the basic premise of this post. Rate cuts are by far the best tool that a central bank has. This tool shouldn't be sidelined just because of the secondary effects on a specific industry, banking. Rate cuts (whether in positive or negative territory) can hurt or buoy the margins in all sorts of industries. But we should still do them because it is the broad macroeconomic effects that we are interested in harnessing.

As for your question about quantitative easing, I spoke to this in my comment in BJH above. Briefly, quantitative easing means that future settlement balances will be massive. And sure, that is a bit stimulative. But who cares? A future central banker can reverse all of this by simply raising the central bank's deposit rate. The sum total of settlement balances in the system may seem large, but it is mostly meaningless.