If you've read this blog for a while, you'll know that I like to talk about monetary technology. Unlike financial technology, monetary tech involves a technological or sociological upgrade to the monetary system itself. And since we are all unavoidably users of the monetary system—we all think and calculate in terms of our nations unit of account—each of us is immediately affected by the change.During the bimetallic debates of the late 1800s, one of the more interesting compromises put forward was Nicolas Veeder's cometallic standard. His model 'Republic of Eutopia' coins (1866) had a plug with 12.9 grains of gold and ring with 206¼ grains of silver. A good idea or no? pic.twitter.com/6eZN2YAq6o— JP Koning (@jp_koning) May 28, 2018

Veeder's Eutopia coin is an old monetary technology that was never adopted. More recent examples of unadopted (or as-yet not adopted) montech include Fedcoin, NGDP futures targeting, or Miles Kimball's technique for evading the zero-lower bound, which would decouple the value of paper money from electronic money. Examples of recent monetary tech that went on to be adopted include the switch from paper to plastic banknotes, the replacement of older end-of-day clearing systems to real time gross settlement systems, and inflation targeting.

Fintech is more limited in scope than monetary tech. Only that portion of the population that uses these innovations is affected—everyone else's financial habits continues on as before. Recent examples include bitcoin, p2p lending, and roboadvisors. (If bitcoin ever became the standard unit of account, it would have made the trek over to becoming monetary technology, and not just fintech.)

-------------

In that context, a broad popular movement for the remonetization of silver emerged. Prior to being on gold standards, nations were generally on a pure silver standard or a bimetallic standard. On a gold standard the debtor class had only one way to settle the debt, by providing the proper amount of gold coins. But if silver coinage was reintroduced at the old rate of sixteen-to-one, debtors could instead sell their labour to buy cheap silver, have it minted into legal tender silver coins, and use those silver coins to pay off the debt. Paying their debts with silver rather than gold meant they'd have a bigger amount of wealth remaining in their pocket.

The movement to restore bimetallism wasn't purely a populist one. The smartest economists of the time--folks like Irving Fisher, Leon Walras, and Alfred Marshall--also preferred bimetallism. A bimetallic standard recruits more monetary material into service than a gold standard. This is advantageous because, as Fisher put it, it "spreads the effect of any single fluctuation over the combined gold and silver markets." In other words, the evolution of the price level under a bimetallic system should be more stable—and thus more fair—than under a monometallic system, since it can absorb larger shocks.

The problem with bimetallism is that it very quickly runs smack into Gresham's law. The traditional way to bring the two metals into service as monetary material was to offer to mint both high denomination gold coins and lower denomination silver coins. So if a merchant needed £20 worth of coins, he could bring either a chunk of raw gold to the mint, or an even bigger chunk of pure silver, and the mint would convert either chunk into £20 for him. The specified amounts of raw silver or raw gold that were required to get a certain number of £-denominated coins constituted the mint's official gold-to-silver exchange rate.

Inevitably the market's gold-to-silver exchange rate would diverge from the mint's official exchange rate, effectively over- or undervaluing one of the two metals. In this situation, no one would bring any of the overvalued metal to the mint to be turned into coins. After all, why bother minting a chunk of gold (assuming the yellow metal was the overvalued one) into £20 worth of coins if that same amount of gold has far more purchasing power overseas? The overvalued metal would thus disappear as it was hoarded and exported, leaving only the undervalued metal in circulation. A monometallic standard had accidentally emerged, and all the benefits of bimetallism were for not.

To prevent Gresham's law from being engaged, the mint had to constantly adjust its official rate so that it stayed in-line with the ever-evolving market rate. Not only would these changes have been politically costly, but they would required an expensive series of recoinages in order to ensure that coins always had the proper amount of silver or gold in them.

--------

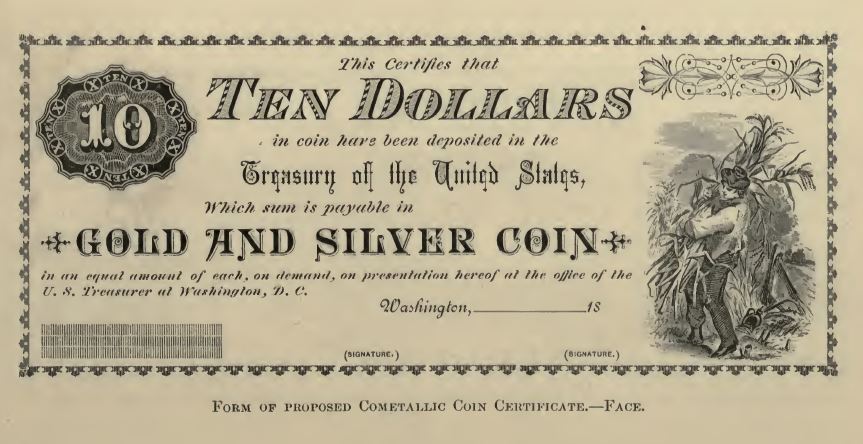

Rather than defining a dollar as simultaneously a fixed amount of gold OR a fixed amount of silver, Veeder's pamphlet suggested defining it as a fusion of the two together. Specifically, Veeder's dollar was to contain 12.9 grains of gold AND 206.25 grains of silver. It's worth noting that under a proposed cometallic standard, paper dollars needn't be redeemed with actual Eutopia coins, but could be converted into separate silver and gold bars or coins. The important rule was that each dollar's worth of debt had to be discharged with 12.9 grains of gold and 206.25 grain of silver.

|

| A model of a cometallic gold certificate, from page 60 of Veeder's pamphlet on cometallism |

Veeder's cometallic scheme was a neat way to keep all the benefits of bimetallism with none of its drawbacks. Cometallism would draw on the combined supplies of the gold and silver markets, so that the system would be much more elastic than a pure gold standard, and thus fairer to both creditors and debtors. At the same time, Gresham's law would be avoided. Under traditional bimetallic coin systems, the mint established an exchange rate between the two metals. This rate inevitably became the system's undoing when it diverged from the true rate.

But a mint that was operating under a cometallic standard would only accept fixed quantities of silver AND gold before it would mint a $1 coin, and so it would no longer be setting an exchange rate between the two precious metals. The undervaluation of one of the metals, a key ingredient for Gresham's law, could never emerge under cometallism.

---------

"I propose that currency should be exchangeable at the Mint or Issue Department not for gold, but for gold and silver, at the rate of not £1 for 113 grains of gold, but £1 for 56^ grains of gold, together with, say, twenty times as many grains of silver. I would make up the gold and silver bars in gramme weights, so as to be useful for international trade. A gold bar of 100 grammes, together with a silver bar, say, twenty * times as heavy, would be exchangeable at the Issue Department for an amount of the currency which would be calcalated and fixed once for all when the scheme was introduced. (It would be about .€28 or .€30 according to the basis of calculation)."Marshall's proposal was later dubbed symmetallism. (I wrote about it here.) If you study monetary systems, you'll run into the gold & silver basket idea sooner or later. The concept is invariably refereed to as symmetallism (and not cometallism) and attributed to Marshall (not Veeder). In the 1800s academics were not required to provide references, and from what I understand plagiarism was rampant. Did Marshall develop his idea separately from Veeder, or did he rip it off? Whatever the case, Veeder was an unknown executive at a small manufacturing concern, whereas Marshall a world famous academic. Celebrity carried the day.

---------

Hubbell owned the patent to the goloid alloy, so he would have made a good profit if the goloid dollar had been adopted by the U.S. Treasury. Unlike Veeder, Hubbell doesn't seem to have been a very good monetary economist, and the case he makes for goloid misses much of nuances of the benefits of bimetallism and the hazards of Gresham's law. He lists a number of advantages for his proposed coin, including: superior durability to gold and silver coins; not susceptible to oxidization (unlike silver); a goloid dollar was smaller than a silver dollar and thus more convenient for consumers to carry around; the mint would be able to make more goloid dollars than silver dollars with its existing capacity; and goloid coins could not be easily melted down for usage in the arts as was the case with gold and silver coins.Another proposed fix was William Hubbell's "goloid" metric dollar (1878). This specimen is 1 part gold, 16.1 parts silver, and 1.9 parts copper. Whereas Vedeer's dollars kept the metals apart, Hubbel's intermingled them. https://t.co/qXpE7EbQrk pic.twitter.com/csNahz1Hhq— JP Koning (@jp_koning) May 29, 2018

Hubbell's idea foundered on the fact that a goloid coin, despite containing gold, has almost the exact same colour as a silver coin. Hubbell's critics believed this set the coin up to be widely counterfeited. A counterfeiter could make a replica with lower gold content, this alteration unlikely to be noticed by the public since the colour of a genuine goloid coin and the fake would be the same.

The difficulties that Hubbell experienced alloying gold and silver were not lost on Veeder. In has pamphlet he mentions that "my first approach, as with many other persons, was to combine the two metals as an alloy for coinage, but, owing to certain difficulties... this idea was soon considered impracticable and abandoned." To avoid Hubbell's color problem, Veeder ended up mechanically wedding the two metals rather than chemically combining them, the Eutopia coin being comprised of a ring of silver and a gold plug embedded inside.

--------------

Today, most western central banks define the national currency in terms of a basket of consumer goods and services rather than a fixed amount of gold (gold monometallism) or a basket of gold & silver (cometallism, symmetallism). This makes a lot of sense. If we want to create a stable monetary standard, one that provides creditors and debtors with an even playing field, better to use a broad basket of stuff that regular people buy than a narrow basket of metals. That way all parties to a contract know many years ahead of time exactly how much consumer goods they will get (if they are creditors) or give up (if they are debtors). Knowing how much gold and silver baskets they will owe or be owed is less relevant to the average person, since gold and silver are a very small part of most people's day-to-day consumption profiles.

There is an important debate going on today about whether to continue defining national currencies in terms of a consumer goods & services basket, or whether to move to something more fluid like a nominal gross domestic product (NGDP), or output. One problem with using a consumer goods basket is that, in the event of a large economic shock that leads to significant loss of jobs, debtors take on all the macroeconomic risk. After all, they owe just as many CPI baskets as before, but have less capacity to meet that obligation because they might not have a job. This doesn't seem like a fair splitting up of risks and rewards.

The nice thing about defining the national currency in terms of NGDP, or output, is that the risk of a large shock, and the associated loss of jobs, is shared between creditors and debtors. This is because if a recession occurs, debtors will owe a smaller amount of real wealth to creditors than they otherwise would. And during a boom, when the job offers are rolling in, creditors will owe more.

Cometallism was never adopted. Perhaps it was a bit too fancy. NGDP is a bit exotic too, but then again so were many forms of monetary technology, until they were actually adopted and became part of the background. We'll have to see what happens.