I recently wrote two posts for the Sound Money Project about Swedish monetary innovation. The first is about an effort by the Swedish central bank—the Riksbank—to force retailers to accept cash, and the other is about the e-Krona, a potential Riksbank-issued digital currency.

This post covers a third topic. For many years now those of us who are interested in cash, privacy, and payments have had our eye on Swedish banknote demand. The amount of paper kronor in circulation has been declining at a rapid pace. Many commentators are convinced that this is due to the rise of digital payments. Since Sweden is at the vanguard of this trend, it is believed that other nation's will eventually experience similar declines in cash demand too.

But I disagree. While digital payments share some of the blame for the obsolescence of paper kronor, the Riksbank is also responsible. The Riksbank betrayed the Swedish cash-using public this decade by embarking on an aggressive note switch. Had it chosen a more customer friendly approach, Swedes would be holding a much larger stock of banknotes than they are now. As long as other countries don't enact the same policies as Sweden, they needn't worry about precipitous declines in cash demand.

Banknotes are dead, long live banknotes

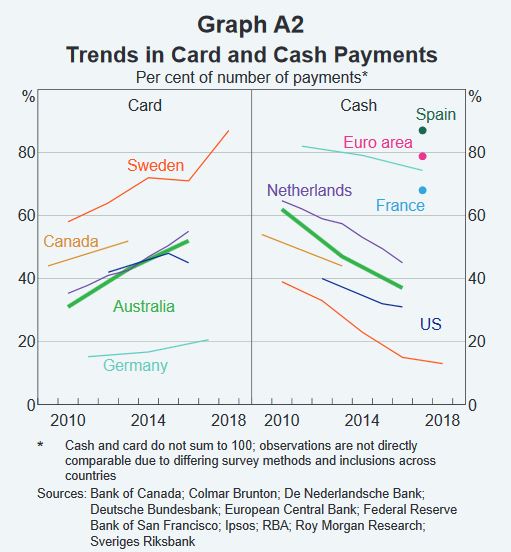

Across the globe, an odd pattern has played out over the last decade. The proportion of payments that are being made with cash has been rapidly declining thanks to the popularity of card payments. Sweden is no different in this respect, although it may be further along than most:

|

| Source: Reserve Bank of Australia |

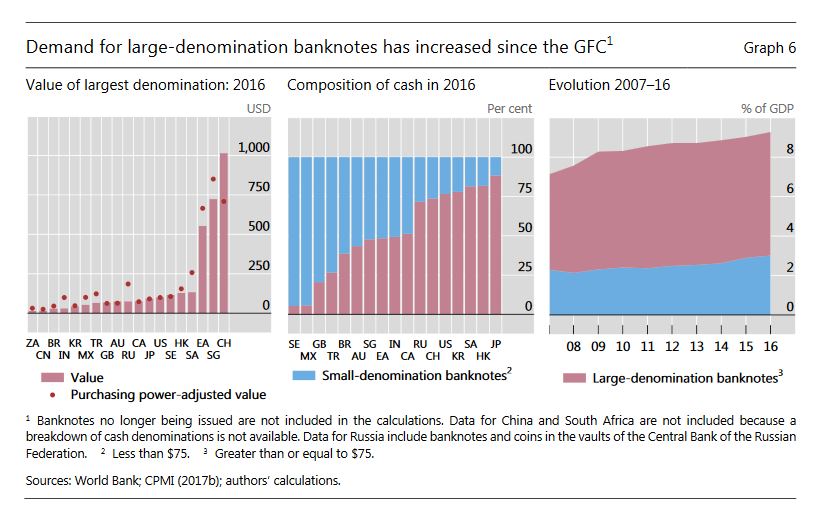

Oddly, even as developed countries are seeing fewer transactions completed using cash, the quantity of banknotes outstanding has jumped. This increase in cash outstanding, which generally exceeds GDP growth, is mostly due to an increase in demand for large-value denominations, as the chart below illustrates:

|

| Source: Bank for International Settlements |

The BIS has a good explanation for this seemingly contradictory pattern. The demand for cash can be split into two buckets: means-of-payment and store-of-value. Banknotes earmarked as a means of payment are generally spent over the next few days. Demand for this type of cash is stagnating thanks to increased card usage. Not so the former. The demand to store $100 bills under mattresses and in safety deposit boxes in anticipation of some sort of disaster is booming. According to the BIS, this is due in part to low interest rates, which makes banknotes more attractive relative to a bank deposit or government bond.

The number of banknotes held as a store-of-value demand accounts for quite a large proportion of total cash in circulation. In a recent paper, Reserve Bank of Australia researchers estimated that 50% to 75% of Australian banknotes are hoarded as a store of value. Keep in mind that these sorts of calculations are subject to all sorts of assumptions. Australia's experience with cash probably applies to most other developed nations.

Sweden, a sign of what's to come?

Which gets us back to Sweden. Sweden differs from all other nations because of what is happening with its banknote count. The quantity of paper kronor outstanding has been consistently plummeting for a decade now, and currently clocks in at just half its 2008 tally:

Surprising, but for the first time in years, the number of Swedish krona banknotes in circulation is growing.— JP Koning (@jp_koning) November 6, 2018

Has Sweden's push to become a cashless society come to an end? pic.twitter.com/T6l1q40Ssu

Even Norway, which has probably proceeded further along the path of digital payments than Sweden, has experienced only a small decline in notes outstanding, nothing akin to Sweden's white-knuckled collapse. The key question is this: why have most developed nations experienced digital payments renaissances along with stability in cash demand, whereas Sweden's own renaissance has been twinned with a seismic drop in cash demand?

The answer to the question is important. Many commentators (including Ken Rogoff) are convinced that the rest of the world's nations will eventually find themselves in the same situation as Sweden. The allure of digital payments will inevitably lead to an all-out Swedish-style desertion of cash.

I'm not convinced. As I mentioned at the outset of this post, the Riksbank shot itself in the foot by carrying out an aggressive currency swap between 2012-2017. This swap did incredible damage to the paper kronor "user experience", or UX. In response, discouraged Swedes fled from cash and substituted into less awkward alternatives like bank deposits. Let's take a closer look at Sweden's 'great note switch'.

The 'great' note switch

Every decade or two central banks will roll out new banknotes with updated designs and anti-counterfeiting measures. This is good policy since it cuts down on fake notes. These switches are generally carried out in a way that ensures that the public's user experience with cash remains a good one throughout. The best way to maintain cash's UX during a changeover period is to allow for long, or indefinite periods of concurrent circulation between old and new notes. Concurrent circulation cuts down on confusion and hassle endured by note users.

Let me explain with an example. Up here in Canada, the Bank of Canada introduced polymer banknotes between 2011 and 2013. But no time frame was placed on the demonetization, or cancellation, of previous paper $5, $10, $20, $50, and $100 notes. Since we all knew from the get-go that we would be free to spend or deposit old Canadian banknotes whenever we got around to it, we didn't have to go through the hassle of rounding up old notes stored under our mattresses and bringing them in for new ones. Apart from the novelty of polymer notes, we hardly noticed the switch to polymer.

Not so with Sweden's rollout of new banknotes. Rather than allowing for a long period of concurrent circulation between old and new notes, the Riksbank announced a shot-gun one-year conversion window for legacy notes. After that point, all old notes would be declared invalid.

For instance, the new 20, 50, and 1000-krona notes were all introduced on October 1, 2015. Swedes had until June 30, 2016—a mere 273 days later—to spend the old notes at retail outlets, after which it was prohibited for retailers accept old notes. If they had missed that window, the Swedish public then had another 62 days—till August 31—to deposit them in banks. After that, all old 20, 50, and 1000 notes would invalid. Owners of invalid banknotes could bring them to the Riksbank, fill out a form explaining why the due date had been ignored, and for a fee get valid ones.

The same shot-gun approach characterized the rollout of the new 100 and 500 the following year. Swedes had 273-days to spend old 100 and 500-krona notes, and another 365 days to deposit them at banks.

I've pasted the time frame for the entire conversion below:

|

| Source: Riksbank |

The October 2015 and 2016 switches were preceded by a preparatory demonetization in 2012. At the time, Sweden had two types of 1000-krona note in circulation. The version that had been introduced in 2006 had a special foil strip to combat counterfeiters, but the 1989 version did not. In November 2012 the Riksbank announced that Swedes would have 418 days—till Dec 31, 2013—to use old 1000 notes without foil strips. After that date the notes would be invalid.

That outlines Sweden's hectic changeover timeline. Now, let's go back to 2012 and put ourselves in the shoes of Hakan, a Swede who has stashed a few 1000-krona banknotes in anticipation of emergencies or other exigencies. In 2012, Hakan would have learnt that all of his 1000-krona notes without foil strips would have to be replaced or declared invalid.

How to deal with this annoyance? Hakan could have replaced them with 1000-krona notes with foil strips, but the Riksbank had also communicated that notes with strips were to be invalidated by 2016. Replacing them with 500 notes would be equally inconvenient, since these were scheduled to be replaced in 2017. Rather than committing himself to a string of inconvenient switches, Hakan may have simply given up and deposited his notes in a bank.

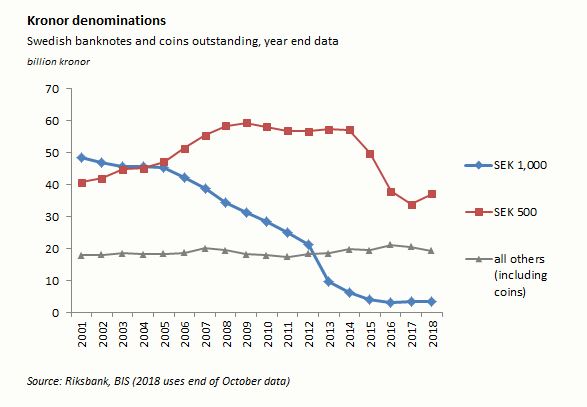

Below I've charted the evolution of Sweden's notes-in-circulation by denomination:

Note the massive 50% decline in 1000-krona notes outstanding between the end of 2012 and 2013. Granted, the 1000-krona was already in decline prior to then. But without the aggressive 2012-13 demonetization, this decline would have been much less precipitous.

Even more glaring is the drop in the number of 500-krona notes beginning in 2015 as the conversion period approached. Rather than swapping old 500-krona notes for new ones, or 1000-krona notes, Swedes instead choose to deposit them in the bank. After enduring a stream of inconvenient note exchanges, were cash users like Hakan simply sick of their product expiring on them?

A natural experiment: Norway v Sweden

Neighbouring Norway serves as a good control or benchmark for studying Sweden. Both nations have similar tastes for digital payments and cash, identical banknote denomination structures, and their currencies trade close to par. But unlike Sweden, Norway did not implement a massive note replacement effort. This gives us some clues into how Sweden's switch may have affected demand for the paper kronor.

Below I've separately charted the evolution in the value of each nation's stock of 500 and 1000 notes, and the combined large denomination note stock (1000s + 500s).

During the 2015-2017 changeover period, demand for Sweden's 500-krona note plummeted, but uptake of the Norway's 500-krone note continued to grow nicely (first chart). The aggressive demonetization of 2012-13 coincided with a big drop in the quantity of Swedish 1000-krona notes. Meanwhile, the rate of decline in the quantity of Norwegian 1000-krone notes continued as before (second chart). What message do I take from these two charts? Given two otherwise equal nations, the one that subjects its citizens to an aggressive note swap will experience a large decline in the popularity of the targeted note.

As for the last chart, the total value of Swedish high denomination banknotes was once twice that of Norway's count. But it is now equal to that of Norway, despite the fact that Sweden has twice the population. My guess is that if the Riksbank hadn't inflicted a series of aggressive demonetizations on Swedes, folks like Hakan could have blissfully ignored the entire changeover, and Sweden would still have a much bigger note count than Norway. The black dotted line gives a hint of where Sweden might be now if the pre-changeover trend in kronor banknote demand had continued.

Why did the Riksbank betray the Swedish public?

Why didn't the Riksbank adopt the same policy as the Bank of Canada during its own massive note switch? In the charts above its quite easy to point out when the 500-krona and 1000-krona notes were replaced. But try spotting when Canada switched from paper to polymer banknotes:

You can't, because it was a gentle switch, one that didn't hurt cash's UX.

Patriotic Swedes might counter that Sweden isn't Canada, it has its own way of doing things. But during previous Swedish note introductions, long windows of concurrent circulation were the standard. For instance, when the 1000-krona note that was printed from 1952-1973 was replaced by a new 1000 note in 1976, the legacy note remained valid for more than ten years after that, until Dec 31, 1987. And when the next series of 1000-krona notes was rolled out in 1989, the legacy note was accepted until December 1998. Long windows, not short ones, is the Swedish tradition.

A March 2018 report from the Riksbank entitled Banknote and coin changeover in Sweden: Summary and evaluation gives some insights into why a shot-gun switch was chosen instead of a user-friendly approach. Very early on the process, the Riksbank began to consult with firms involved in the movement of cash including the BDB Bankernas Depå AB (a bank-owned cash depot operator), the Swedish Bankers’ Association, the larger banks, ATM operators, and others. One of the questions that was discussed was how long the old banknotes should remain valid. In April 2012, these market participants submitted their preferred timetable for the changeover. One of their preferences was for:

"...the old banknotes and coins to become invalid after a relatively short period so that they could avoid having to manage double versions of the banknotes and coins for an extended period."These same market participants also requested that the Riksbank demonetize the old 1000-krona notes without foil strips. Removal of this older series meant one less version to manage once the new 1000-krona note was debuted in 2015. Market participants also hoped that the old banknotes wouldn't be exchanged for new ones, thus reducing the total amount in circulation. If you are wondering why bankers might want fewer banknotes outstanding, go read my 'conflict of interest' section a few paragraphs below.

The timetable that ended up being adopted by the Riksbank in May 2012 was basically the same one proposed by industry. So there you go. The Riksbank introduced a shot-gun approach because that's what Swedish bankers wanted. But in designing the changeover to be convenient for banks, the Riksbank threw the Swedish public under the bus. Nor was it unaware of the inconvenience it was imposing on Swedes. According to the March 2018 report:

"The Riksbank was aware that the timetable would lead to complications for the general public in that there would be a number of different dates to keep track of. The need for information activities would be increased. However, the Riksbank considered that the interests of the cash market were more important..."Now, if the Riksbank had justified the shot-gun switch as a way to flush tax cheats out, I might be more sympathetic. At least an argument could be made that the public's welfare was being served by imposing a series of inconveniences on them. But as the above quote indicates, the motivations for quickly invalidating old notes was much less nuanced than this. The Riksbank deemed that the 'complications' that the general public had to endure simply weren't as important as the 'interests' of the banks. Full stop.

There is a huge conflict of interest involved in consulting with banks about cash's future. Sweden's bankers would have been quite pleased to provide the most awkward timetable imaginable. After all, they would have been the main beneficiaries. The more Swedes who forsake cash to pay with cards, the more fees banks earn. Furthermore, each kronor that is held in the form of cash is a kronor that isn't held at a bank in the form of a deposit. Banks lust after consumer deposits because they are a low-cost source of funding. One wonders if the Riksbank fully understood this conflict of interest.

Notes for the future

The decline in the kronor count has finally been reversed. In the tweet I embedded above, the amount of paper kronor in circulation rose in 2018, the first increase in many years. The impositions on the the kronor's UX over the last five years are finally drawing to a close. Now that they no longer have to worry about timetables and expiry dates, are Swedes like Hakan finally returning to the market?

The great irony is that the Riksbank, having caused a big chunk of the decline in 1000 and 500-krona note usage, is suddenly getting quite worried about this trend. Earlier this year, Riksbank governor Stefan Ingves lamented that

"There are those who think we have nothing to fear in a world where public means of payment have been replaced completely by private alternatives. They are wrong, in my opinion. In times of crisis, the general public has always sought refuge in risk-free assets, such as cash, that are guaranteed by the state. The idea of commercial agents shouldering the responsibility to satisfy public demand for safe payments at all times is unlikely."The Riksbank may even roll out an e-Krona, a digital currency designed to meet Swede's desire for "continued access to a means of payment that is risk-free and guaranteed by the state." Odd that Ingves is now so concerned about Swedish access to a risk-free payments medium when he was so willing to ignore the interests of Swedish cash owners just a few years before.

Sweden will probably have to go through another note switch sometime in the late 2020s. I hope that when it comes, Swedish bankers will get a little bit less representation at the table and the Swedish public a bit more.

As for concerned citizens and central bankers in other countries that are planning to introduce new notes, we can all learn some lessons from Sweden's 2012-2017 changeover. Aggressive note switches may be good for private bankers, but they hurt cash-using citizens. The long-window approach to note switches, not Sweden's shot-gun method, is the customer-friendly approach.

Dedicated to my favorite Swedish hockey player: