|

| By Harcourt Romanticist [source] |

This post is dedicated to the protesters in Hong Kong. I am awed at how courageous they have been in the face of continuing pressure from China's Communist party. The same regime is complicit in

persecuting Uighur Muslims and imprisoning

two Canadians, Michael Spavor and Michael Kovrig.

There are all sorts of creative forms of non-violent mischief that citizens can use to protest against oppressive governments. This post explores a sub-category of non-violent mischief:

monetary mischief.

Money stamping

One of the most popular forms of monetary protest is to overstamp currency. This involves stamping banknotes or countermarking coins. Coins and banknotes are vital to trade and circulate widely. Which makes them a great way to advertise a cause or complaint. The message automatically propagates itself via hand-to-hand commerce.

The monetary authorities will react to the threat by hastily withdrawing marked notes and coins from circulation. When bills or coins enter the wholesale cash system

—i.e. when they are collected by banks, cash-in-transit firms, or ATM companies

—they are typically sorted by machines (or hand) for fitness. Defaced currency will get filtered out and returned to the central bank (or mint) to be destroyed and replaced.

This form of protest goes far back in history. For instance, below is a photo of a 1903 penny that has been defaced with a suffragette rallying cry:

|

| "It was said at the time, that the suffragettes had copied the practice from anarchists, who were defacing similar coins with the phrase ‘Vive l’Anarchie’." Source: British Museum |

Wayne Homren, editor of

E-Sylum, has recently explored some modern U.S. examples of money stamping as protest:

Here are

a few examples from Ireland during the Troubles:

|

| © Fitzwilliam Museum. "The one illustrated in Figure 6 is a 1971 UK two-pence which has been stamped with ‘SMASH H BLOCK 8' on the obverse bust. The H-blocks at the Maze/Long Kesh prison housed prisoners convicted of scheduled offences after 1 March 1976, with H-block 8 reserved for IRA prisoners. The hunger strikes of 1981 came in protest at the removal of Special Category Status from prisoners and led to the deaths of ten IRA hunger strikers." Source: Richard Kelleher, Money and Medals Newsletter 77 |

Hong Kongers still use plenty of cash. Which would seem to make Hong Kong ideal for money stamping. However, I haven't seen many examples of this form of mischief being used by Hong Kong protestors. About the

only evidence I've located is provided below. It is a warning from a Thai money changer that it will not accept Hong Kong notes that have been stamped with political messages:

Which leads directly into my next point. For every form of monetary mischief, the authorities have a defence. The simplest line of defence against overstamping is to declare the practice illegal. Luckily for protestors, it is almost impossible to enforce this law. Money stamping can be safely performed behind closed doors. If a money stamper is caught passing along a note or coin, they can just say they accidentally received it as change or from an ATM.

A more effective line of defence is to declare that any stamped banknote is henceforth no longer money. This is basically a form of

demonetization, a very focused one. To initiate this defence, the central bank refuses to accept any note or coin that has been altered. Good bills can continue to circulate. If the central bank refuses to accept marked bills, then wholesalers like banks (and forex dealers like the Thai one above) will likewise refuse, and so retailers won't accept it. And so angry members of the public who have stamped their notes with protest messages will find that their cash has become unspendable.

To avoid being left out of pocket, protesters will avoid stamping their currency in the first place. Which is why this line of defence is fairly effective.

Small, not large denominations

Protestors have a good counter to the threat of demonetization. They can focus on stamping large amounts of small denominations, not small amounts of large denominations. In Canada and U.S., the relevant small denominations are $1 coins/bills, $2s, and $5s. In Hong Kong's case, the relevant small denominations would be the HK$10 and HK$20 notes, which are equal to around US$1.20 and US$2.40 respectively.

There are two reasons for focusing on small notes. First, it is far safer for a student protestor to overstamp a few HK$10 notes. If the notes are to becomes unspendable thanks to a demonetization, the protestor may have to do without a meal at McDonald's. But if a protestor stamps a few HK$1000 (US$126) bills and they subsequently becomes worthless, that will be far more damaging to their finances.

The second reason for focusing on small denomination notes is that their supply is much less flexible than larger denominations. Think about it for a moment. For each $500 that a central bank printing press produces, it takes fifty times the effort to create an equivalent amount of $10s. Which means that it will be harder for the central bank to replace a large amount of defaced $10s than to replace an equivalent value of defaced $500s.

This difference in replacement rates is important. When notes that have been stamped with political slogans are declared void by the monetary authorities, the supply of banknotes will be reduced. A shortage has been created. The central bank can quickly remedy a shortage of large denominations like HK$500s. But fixing a shortage of HK$10s will take more time. The monetary authorities are left with a choice. They can either allow the shortage of small denomination notes to continue, or they can bring it to an end by re-allowing defaced notes to circulate.

Either way, the government ends up looking bad. Shortages of change are extremely inconvenient to businesses. Those in charge will be derided as incompetent. But allowing small denomination defaced notes to return to circulation will allow the protesters to continue advertising their cause.

Cashing out of bank accounts

A second form of monetary protest is mass cash-outs of bank accounts. In 2010 Eric Cantona, a former French footballer, started

to champion this form of mischief. I'm pretty sure he wasn't the first to come up with the idea. (Anyone else have prior examples?). Anyways, here he is:

"We don't pick up weapons to kill people to start the revolution. The revolution is really easy to do these days. What's the system? The system is built on the power of the banks. So it must be destroyed through the banks.

"This means that the three million people with their placards on the streets, they go to the bank and they withdraw their money and the banks collapse. Three million, 10 million people, and the banks collapse and there is no real threat. A real revolution."

"We must go to the bank. In this case there would be a real revolution. It's not complicated; instead of going on the streets and driving kilometres by car you simply go to the bank in your country and withdraw your money, and if there are a lot of people withdrawing their money the system collapses. No weapons, no blood, or anything like that."

Last January French protestors,

the gilets jaunes, gave it a try.

How effective are mass cash withdrawals?

Banks rely on multiple sources of funding, one of which is its base of retail depositors. They also tap investors (who buy their bonds and shares) as well as depositors from the government and corporate sectors. If a portion of their retail depositors close their accounts, this will probably hurt the banks. But given the diverse nature of bank funding, I think Cantona overplays his hand when describes it as a "really easy revolution."

Banks also have access to the most powerful lender of all, the central bank. If protestors do succeed in pressuring certain banks with a cash-out campaign, the central bank will step in and support the targeted bank by lending it funds. Since the bank is being pressured for political reasons, and not because it is fundamentally unsound, the central bank will be quite liberal in support. Ultimately, central bank support should staunch the run.

Like the

gilets jaunes in France, protestors in Hong Kong have launched their own cash-out campaign

—with a twist. Hong Kong pegs its currency to the U.S. dollar. Not only are protestors cashing out of their bank accounts. They are also converting their Hong Kong funds into U.S. dollars in the hope of pressuring the peg.

I combed through Hong Kong Monetary Authority statistics to see if the cash-out campaign is having any effect. Banks and other financial institutions will typically keep a small amount of banknotes and cash in their vaults to satisfy customer redemption requests. Below I chart out the evolution of the cash held by Hong Kong banks by year.

You can see that Hong Kong banks have currently stocked up on over HK$30 billion in currency, far more than the typical HK$20 billion they tend to hold in August. This amount exceeds the Christmas spike, when the public typically withdraws the largest amounts of cash for purposes of gifts and travel. (Apparently the early 2018 jump may have been related to the

installation of facial recognition hardware on neighboring Macau's ATMs).

It's hard to say why cash inventories have spiked. It could be related to banks being worried about protestor-led cash withdrawals. Or alternatively, they may fear that even non-protestors may start to ask for cash-outs, albeit for economic reasons, not political ones.

As I said earlier, I think that cash-out campaigns probably won't have a big effect. Banks have very strong lines of defence. As for attacking the Hong Kong dollar peg, that's quite ambitious. In theory, it would work. But every depositor in Hong Kong would have to participate.

Again, focus on small denominations

If I was to start a monetary protest here in Canada that involved cash withdrawals, I'd set my ambitions lower. The way to make any cash-out campaign more effective is to focus on withdrawing small denomination notes. Go into the bank and ask to withdraw $1/$2 coins and $5 notes. (In Hong Kong, HK$10s and HK$20s instead of HK$500s). Or withdraw large denomination notes from ATMs and then go to stores and ask them to break them for you. If the store won't break them, than buy a $1 chocolate bar with a $20 and hoard the change.

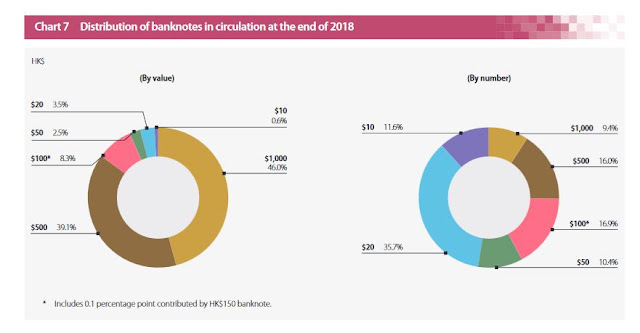

Earlier, I mentioned that the supply of small denomination notes is not as elastic as the supply of large ones. By way of illustration, I've provided a screenshot of Hong Kong's cash supply:

|

| Source: Hong Kong Monetary Authority annual report [link] |

Like most countries, Hong Kong has far more small denomination notes and coins in circulation than large ones. As the chart on the right shows, the HK$10 and HK$20 constitute 11.6% and 35.7% of all bills in circulation. But the total value of these small denomination notes tends to be quite small, as the left chart illustrates. They comprise just 0.6% and 3.5% of total banknote value. You can see

the same distribution in Canada, too. The value of $100 bills dwarfs the $5 bill, but we've got about the same amount outstanding.

So there are a boatload of small denomination banknotes in circulation that are responsible for bearing a large load of the nation's transactional work. But the combined value of these work-horse notes is quite low.

This set of features makes small denomination currency an easy target for a would-be monetary protestor. A motivated group of Canadians could conceivably hoover up a large share the small denomination note and coin supply, thus creating a shortage of change. If enough people participate, the Bank of Canada's printing press would not be able to keep up. This would impede the ability of the Canadian payments system to facilitate transactions.

Most people have forgotten what small change shortages look like. But anyone who has read a bit of monetary history will know that many of the large monetary disturbances in the last five or six centuries leading up to 1800 were coin shortages. They were a nuisance.

In this post I've explored two types of non-violent monetary mischief that protestors have turned to in the past. I'm sure there are more. For instance, I haven't mentioned any digital types of mischief. In the comments below, feel free to provide some examples. As for the Hong Kongers who my be reading this, I wish you the best. Hang in there.