The only type of central bank-issued money that we hoi polloi can own are banknotes. But over the last few years, researchers at central banks have been increasingly toying with the idea of issuing digital money for public consumption. I count 380,000 search results on Google for the term "central bank digital currency," up from zero just a few years ago.

There are two types of proposed central bank digital currencies, or CBDCs. The first, Fedcoin, is implemented on a blockchain. I wrote about it here. But the odds of Fedcoin happening are minuscule. This post will be about the second type.

The second is a basic bank account, sort of like PayPal except run by a central bank like the Federal Reserve (or the European Central Bank or the Bank of England.) Just like you go to PayPal's website to register for an account, you'd head over to the Fed's website to open an account. A Fed version of PayPal would let you pay your friends, accept donations and business income, and buy stuff at stores. Except you'd be using Fed money, not PayPal money.

I'm not philosophically or ideologically opposed to the idea of a Fed PayPal. If the Fed (or any other central bank) wants to get into providing payments services to regular folks, fine. The same goes for Walmart. If it wants to start providing retail bank accounts, great. Ditto for Facebook. I think Libra is an admirable project. Oh, and I also want more co-operative banks and credit unions. What about community currencies? By all means, let's get more alternative systems like Ithaca Hours and the Bristol Pound up and running. And while were at it, commercial banks, credit unions, and municipalities should be allowed to issue banknotes. Heck, why not a Nike banknote?

In short, the more payments options people have, the better. (My one caveat: If a central bank is going to introduce a central bank version of PayPal, it should be obligated to recover its costs. FedPal shouldn't have an advantage over regular PayPal, the Michigan First Credit Union, or a commercial bank like Wells Fargo.*)

All that being said, I'm not terribly optimistic about the prospects for a central bank version of PayPal.

With paper money, central banks already have an incredibly popular product. Banknotes are anonymous. People can use them for activities that might be frowned on, and this is a pretty big market. Bills have another nice property; they are ungated. Anyone can accept a dollar without needing to open an account. This accessibility has made paper dollars, which can move fluidly across borders, wildly popular in nations with poorly functioning banking and monetary systems. Most importantly, central banks have a monopoly on the business of issuing cash. So they don't have to worry about competition.

But the success of central banks' cash line of business won't translate into success for a central bank version of PayPal. Given the current state of anti-money laundering regulations, we probably wouldn't be able to open a Fed PayPal account anonymously. Furthermore, it's unlikely that the Fed, or any other central bank for that matter, would open up eligibility to non-citizens living in foreign countries.

So forget about catering to the huge market of anonymity seekers and foreigners who would love to hold a U.S. dollar account directly at the Fed. FedPal would probably be a US-only product. (Likewise, the Riksbank's e-krona would be a Sweden-only product).

But this is a crowded field. Whereas cash is a government-run monopoly, thousands of competitors offer digital payments accounts. Can the central bank differentiate itself from a slew of other digital account options? I'm skeptical.

1. Features?

You've gotta keep in mind that CBDC is a brainchild of macroeconomic theoreticians, not product designers. Macroeconomists don't have any expertise in designing retail banking products. And so I'm not terribly bullish on the Fed or the Bank of England coming up with new features that would differentiate a central bank account from any other payments accounts.

2. Safety?

Not really. In the U.S. (as in most developed countries), bank accounts and prepaid debit cards are already insured up to $250,000. For most regular folks, dollars held at the Fed won't be any safer than those held in banks.

3. Fees?

The Fed might try to offer a low-fee option, perhaps to the unbanked or the underbanked. But in the U.S., this is getting to be a crowded field. Chime, Varo, Ally, and Simple offer no-monthly fee accounts. There are plenty of no-fee prepaid debit cards out there, too. Just last week, I spotlighted the PODERcard, which is marketed to unbanked immigrants.

Nice to see. Green Dot & Welcome Technologies are introducing PODERcard, a debit card targeted to U.S. Hispanic households (14% of which were unbanked in 2017). No monthly fee: https://t.co/T0PGZX5CJ4— John Paul Koning (@jp_koning) May 30, 2020

I've said it before, but competition is the best way to help the unbanked. pic.twitter.com/j2tzQqvVwB

The public sector is already active in this field, too. The Federal government already offers a no-fee prepaid debit card, the Direct Express card, to over 60 million Americans who receive Federal benefits. And state governments often provide no-fee debit cards for tax refunds, unemployment, and other state benefits. It's hard to see what a CBDC can bring to the table.

4. Higher interest rates?

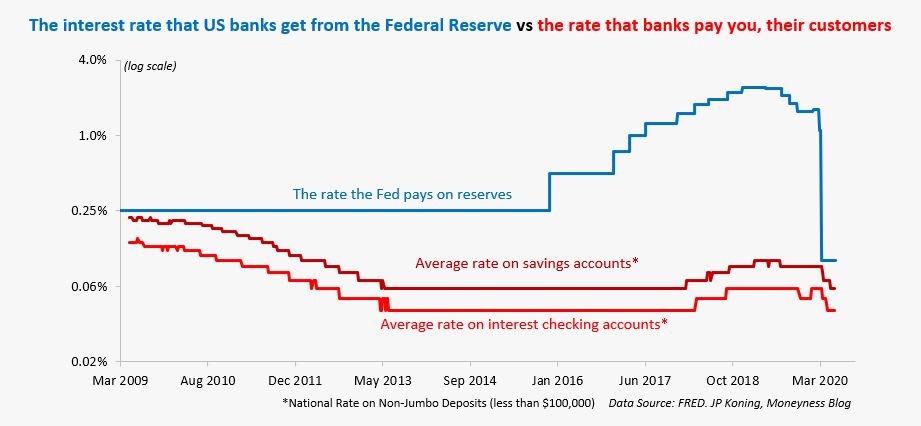

Might a CBDC be able to offer higher interest rates than the competition? A few commentators have suggested that a Fed version of PayPal offer regular Americans the same interest rate that the Fed pays large banks that keep accounts at the Fed. Banks maintain accounts at the Fed so that they can make interbank payments and meet reserve requirements.

In the chart below, the Fed pays banks the blue line, interest rate on reserves. This rate has historically been far higher than the two red lines in the chart: the average rate that banks pay customers on a checking or savings account. (For its part, PayPal pays its customers 0%).

Were the Fed to pay FedPal account holders the blue line, i.e. the same interest rate it pays banks, this would effectively convert a FedPal account into an incredibly high-yield checking account. No doubt it would become a wildly popular product.

But serving millions of retail customers is a lot more expensive than serving a couple of hundred banks. Think customer help lines, fraud prevention, advertising, paper check processing, ATM network fees, and more. As I stipulated at the outset, FedPal shouldn't be allowed to operate at a loss. This would be unfair to the thousands of community banks, credit unions, fintechs, and commercial banks that are trying their hardest to provide payment services to the public.

To recover its costs of serving a retail customer base, the Fed would have no choice but reduce the interest rate it offers. How low would it go? As a monopoly, the Fed is unused to the rigors of competition. I wouldn't expect it to be able to run a tight enough ship that it could afford to pay customers an especially high interest rate.

5. Speed?

Nope. With the introduction of Zelle, it's possible for Americans to make free instant payments, 24/7. Many other nations (like Sweden) also have real-time payments. We've got it here in Canada, too.

--------------

So central bank version of PayPal would be just another middling bank account. Sure, roll it out. But don't expect it to change the world.

Funny enough, central bank macroeconomists are worried about the opposite: that CBDC could change everything. In the papers they write on the topic, macroeconomists fret that any CBDC they introduce will be so attractive that consumers will rapidly desert their regular bank and open an account at the central bank. This would cause the whole banking system to implode.Without a stable base of deposits, banks would be unable do any lending.

In my view, the real threat is the opposite. Given the institutional constraints I listed above, a central bank version of PayPal is destined to be a middling payments product. But it gets worse. Because central bankers are so worried about the macroeconomic effects that a FedPal will have on the economy, they will inevitably underdesign these accounts, turning a middling product into a crappy one. Adoption will never occur, and so FedPal will be wound down. This failure will go on to undermine the reputations of central banks.

The lesson is, either do a stellar job designing these things... or don't do it at all.

* If the U.S. government is going to get more actively involved in offering low cost payments services to the public, there's a better way to get there than starting up a new CBDC-based system from scratch. Just offer government-sponsored prepaid debit cards.

The neat thing is, it already does this. Millions of Americans who receive Federal benefit payments like social security already use the Direct Express card, a no-fee debit card issued by the government in partnership with Comerica. And to help disburse coronavirus relief payments, the government recently issued millions of EIP card, a no-fee prepaid debit card in partnership with Metabank. As I suggested here, why not make these cards better by letting card owners send/receive real-time payments via Zelle, attaching a savings account to the card, and giving users the in-app option of buying Treasury savings bonds.

...A few ways to improve the Direct Express card:— John Paul Koning (@jp_koning) May 1, 2020

-let card owners send/receive real-time payments via Zelle

-attach a savings account to the card

-give users the in-app option of buying Treasury savings bonds

2/2 pic.twitter.com/tLSLfqujWW

In a recent article for the Sound Money Project, I suggested that the IRS start issuing debit cards too.

Great read; generally agree.

ReplyDeleteQuick note: The Fed is required to recover costs for services that it offers under the Monetary Control Act of 1980. The details of the requirement (e.g. when must costs be recovered) are a bit more complicated. The Fed spent a lot of real estate discussing cost recovery for its upcoming FedNOW service in the latest associated Federal Register notice and will likely provide more details in the years to come.

Thanks for that tidbit, Anon.

Delete"The only type of central bank-issued money that we hoi polloi can own are banknotes." Not true, actually.

ReplyDeleteSome countries have state run savings banks, which invest only in reserves and government debt. The UK’s “National Savings and Investments” is an example. Anyone can open an account at NSI.

No cheque books or debit or credit cards are offered by NSI, but money can be extracted and transferred to a standard commercial bank (via phone or internet) in about 24 hours. So NSI is essentially a cumbersome version of a central bank Paypal account.

The really big change would come if a government ceased subsidising commercial banks by offering them taxpayer backed deposit insurance and billion dollar bail outs when they’re in trouble. Certainly there is no excuse for taxpayers to back those who want their money loaned on via a bank, any more than taxpayers should back those who want a stockbroker to lend on or invest their money.

Plus there are plenty of other lenders (mutual funds, peer to peer lenders etc) which are not feather-bedded by taxpayers. Why should those who want a bank to lend on their money be feather bedded?

Abandoning taxpayer support for banks and opening checking accounts for all at the central bank would essentially equal full reserve banking. I wrote some more on that here:

https://mpra.ub.uni-muenchen.de/99989/1/MPRA_paper_99989.pdf

Good points, Ralph. I had forgotten about NS&I. (And of course in many countries, there are still postal banks).

DeleteI am with you on deposit insurance. I have always wondered what the true price of such insurance is relative to the price that FDIC (and other guarantee schemes charge).

JP Koning,

ReplyDeleteI think there is one critical point you haven't mentioned in above comparisons and that is money creation. As we know, most of money exist in the form of deposits. They are created by private banks when they grant loan. Now with FedPal scenario, will CB be allowed to directly issue loan (which in turn creates money) to the public or serve custodial services only ? If CB is allowed to do so, what's the impact for the economy as a whole because it will shift money issuance market shares which is now dominated by private banks.