|

| Bruno Liljefors, 1899, link |

The tax authority and the tax payer are engaged in an age-old cat and mouse game, tax payers trying to perfect tricks that allow them to pay as little tax as possible and the tax authority trying to close these loopholes. Retail cash payments are one of the fields on which this battle is waged. It's interesting to see how sophisticated this cat and mouse game has become.

There are two weak points in the sales process that allow cash-accepting retailers to avoid paying sales taxes or VAT. The first weak point is at the very outset of a payment. When a customer pays with cash, the person behind the till can avoid ringing up the payment. Without a record of the payment having been made, the retailer needn't pay tax.

But even if a retailer rings up all cash payments and provides receipts, they can still avoid paying taxes. At the end of the business day, they need only doctor the cash register's data using a zapper—add on hardware or software designed for this purpose—in effect purging all or a portion of the cash payments registered during the course of business. With the only record of that day's cash payments now being the paper receipts held in customers' wallets—most of which will have been thrown away—the retailer needn't worry about the tax authority discovering the doctoring. (Erasing card based payments is much riskier for the retailer because a paper trail still exists with the card-issuer.)

Tax authorities have been targeting the second point of weakness for a few decades now by requiring retailers to use certified cash registers that have tamper-proof memory units. These are variously known as a fiscal control units, electronic tax registers, or fiscal tills. These tills are designed in such a way that any attempt on the part of the retailer to break into its memory using a zapper or some other technique will be discovered. Additionally, these units have the potential to be connected directly to the tax authority, allowing for instantaneous transmission of sales data and constant real-time tax auditing. That sounds a bit intrusive, no?

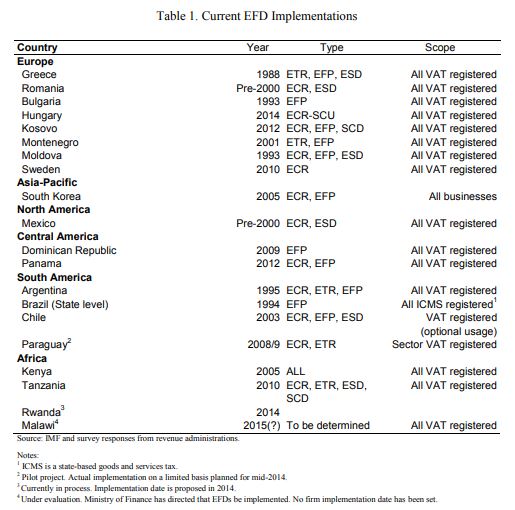

Below is a chart from the IMF showing nations that have implemented fiscal till plans:

|

| Source: IMF, Electronic Fiscal Devices, 2015 |

Progressing to the next stage of the cat and mouse game, retailers will try to evade tamper proof memory units in the cash register by making recourse to the first weak point in the sales process; not entering the transaction into the cash register in the first place. Recognizing this, the tax authorities who have implemented fiscal till schemes have made it illegal to not issue a sales receipt. But illegality doesn't seem to me like a big hindrance to a retailer who has already set their mind on evading taxes.

One neat trick to get retailers to provide receipts—and therefore run all transactions through the tamper-proof cash register—is to recruit the customer into the cat and mouse game as helper. Public information campaigns exhorting people to ask for receipts are one technique. But the more interesting trick is implementing a tax-receipt lottery. All invoices issued from the tamper-proof cash register come with a unique lottery number. Anyone who keeps their invoices will be able to participate in a periodic lottery. Customers thus have an incentive to ask the retailer for a receipt, obliging the retailer to run the transaction through the fiscal till.

Taiwan implemented the first tax receipt lottery back in the 1950s, the Uniform Invoice lottery. I've included a picture below, and here is the website. In the last fifteen years, a number of nations have begun to copy it including Czech, Slovakia, Slovenia, Malta, Portugal, Poland, China, Sao Paulo, and Lithuania.

|

| Taiwan sales receipts with lottery numbers on them |

The next stage of the cat and mouse game occurs as the retailer, desperate to adapt to the government's crafty invoice lottery, tries to coax the customer over to his side. On a $50 meal, a restaurant may be able to save $2.50 in tax (assuming a 5% tax rate) if the the fiscal till is avoided. If the restaurateur says that he will share some of this savings with the customer, he may be able to induce her to not ask for an invoice and thus avoid the till. The amount of money he must dangle in front of her will have be large enough to compensate her for the foregone fun of playing the lottery, potential lottery winnings, and guilt.

China is the most interesting example of the cat and mouse game being played at this level. To incentivize cash-paying customers to ask for invoices, or fapiao, the Chinese authorities have created a scratch and win game. Restaurateurs have reacted by offering customers a free soda, or a discount, if they don't ask for the fapiao. Presumably the value of a soda is just sufficient to compensate the customer for foregoing the lottery. More entertaining accounts of fapiao here and here.

I'm sure these methods of attacking tax avoidance work to an extent. In Québec, for instance, as of March 2016 the tax authorities say that they have recovered CAD$1.2 billion in taxes following the introduction of fiscal tills in the restaurant industry. However, I'll hazard that the biggest determinant of tax avoidance is good government. If people trust the government to do smart things with tax revenues and they don't see evidence of corruption, then they will be more likely to view paying taxes and reporting on cheaters as one of their public duties.

Other sources:

OECD: Technology Tools to Tackle Tax Evasion and Tax Fraud (link)

Ainsworth: Québec’s Sales Recording Module (SRM) - Fighting the Zapper, Phantomware, and Tax Fraud with Technology (link)

Steenbergen: Reaping the benefits of Electronic Billing Machines (link)