The outbreak of Covid-19 has caused a global increase in the amount of cash in the economy. I think I've got a pretty neat explanation for why.

But before I tell you what it is, let me show what the cash build-up looks like. Here's what has happened to banknotes in circulation in Canada so far in 2020:

The quantity of Canadian banknotes in circulation keeps rising. 19 consecutive weeks without a decline. Unprecedented.— John Paul Koning (@jp_koning) July 27, 2020

Any theories? I have one—will write a blog post soon.

(In a counterfactual world without COVID, we'd be at C$94 billion notes outstanding, not $101 billion.) pic.twitter.com/rIWyUqEPnx

Meanwhile, here is the US:

U.S. banknotes in circulation, by year.— John Paul Koning (@jp_koning) July 7, 2020

Usually so predictable, but not in 2020... pic.twitter.com/sdkBvorhtS

And here is the UK:

Each chart shows an unusual increase in banknotes in the economy starting in March or April, when the pandemic first hit western countries. These cash bulges show no signs of shrinking. And they are quite big. In the case of the U.S., I'd estimate that there are $150 billion extra paper dollars in circulation thanks to the virus.There's been a big jump in UK banknotes in circulation since the COVID outbreak started. Oddly, this is happening as ATM cash withdrawals have collapsed by as much as 60%. pic.twitter.com/w3taggoaib— John Paul Koning (@jp_koning) July 31, 2020

I recently came up with a surprising explanation for why this is happening. But before we get to it, we need to review what determines the amount of cash held in the economy. Here's an analogy. Think about how the water level in a reservoir might rise. There are two ways this can happen. More water can run into the reservoir, or less water can flow out. (Conversely, the water level can fall when either less water enters, or more is withdrawn.)

The same principle applies to the amount of cash held in the economy. If more people are taking cash out from ATMs and banks then the amount of cash in the economy will grow. But the amount of banknotes in the economy can also grow without a rise in withdrawals. That can happen when the public (i.e. individuals & businesses) returns less of the stuff than before to ATMs and banks. So more of it stays floating around in the economy.

Now, I must confess that in previous blog posts and tweets I had assumed that the big increase in cash-in-circulation during the pandemic was due to an increase in withdrawals. People were worried about the virus, I thought, so they wanted to take more banknotes out of their bank accounts and hold it under their mattresses. "Cash restocking makes sense in an emergency like the one we are living through," I wrote back in April. And here: "The coronavirus reminds us of the fragility in our infrastructure. And so we rebuild some of our banknote balances."

But now I think that I was wrong. The big increase in cash-in-circulation is not due to an increase in withdrawals of cash. Sure, some people are taking out a few more $50s or $100s to hold under their mattress. But with the virus shutting down the economy, most of us are making less purchases than before. The few transactions that we continue to make tend to be digital, say like buying from Amazon with a card. The net effect is that since March we have been withdrawing far less cash than normal.

If so, then why has the level of cash in the economy jumped? The only explanation is that there is much less cash being returned to banks and ATMs. Businesses and individuals simply aren't redepositing their banknotes. There's some sort of clog or blockade that is gumming up the system and preventing a regular flow of returns. I'll try and explain the precise nature of this clog, but first lets look at some data that confirms that returns of cash have dried up.

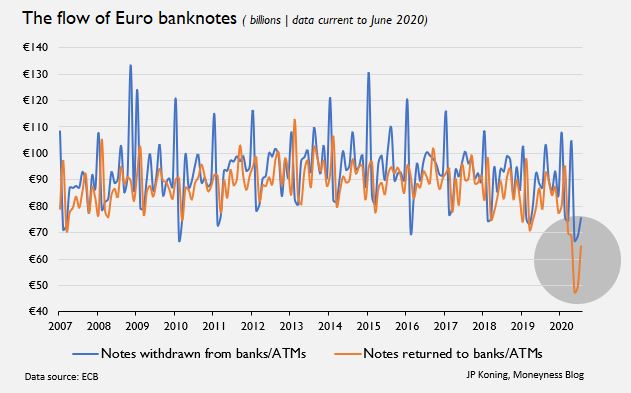

The European Central Bank (ECB) is unique. Most central banks only provide public data on the net amount of cash that is in circulation. But the ECB goes the extra step and offers data on both the flow of banknotes being issued into the economy and the flow being withdrawn from the economy. And so we can actually see which half of the equation is responsible for the big jump in cash: more withdrawals or less returns.

As you can see, Europe has seen a large and anomalous jump in cash-in-circulation in 2020, just like Canada, the US, and UK. I've charted this below:

Now let's see what the ECB's disaggregated data has to say:

In general, withdrawals of euro banknotes (the blue line) has exceeded returns (the orange line) from 2007 to 2020. That's why the amount of cash in the European economy has generally increased over time. During the 2008 credit crisis, there was a big jump in withdrawals, no doubt to worries about the safety of the banking system. But during the pandemic, cash withdrawals (blue line) have actually fallen, not increased. In fact, the level of withdrawals is at its lowest point in over a decade!

Returns of cash (orange line) have plunged by even more than withdrawals. They are at their lowest level ever!

So what does this mean? Thanks to the pandemic, European individuals & businesses have become less interested in taking cash out of the bank. But they are even less interested in returning cash to the bank. It is this outsized collapse in returns, the orange line, that is causing the big build-up in euro banknotes in circulation.

For those who like analogies, let's revisit our reservoir imagery for a moment. The amount of water (i.e. cash) flowing into the reservoir (i.e. the economy) has slowed to a trickle. Normally this trickle would lead to a fall in the water level. But because even fewer people are removing water (i.e. doing cash returns) from the reservoir, the incoming trickle is sufficient to push the water level higher.

I think there's a good chance that what is happening in Europe is happening in the U.S., Canada, and U.K. too. Thanks to the virus, no one is redepositing their banknotes. But I'd have to see the data to be sure.

Now we can finally get to my theory for what is clogging up the system. The peculiar feature we need to explain is people are so much less willing (or able) to return their notes during the pandemic than they are willing to withdraw them. Or put differently, why did the orange line fall so much more dramatically than the blue line did? It suggests some sort of asymmetry in people's usage of cash. My theory is that this asymmetry can be found in the nature of the black market, illegal drug markets, the mob, the underground economy, etc.

The specific asymmetry is this: it is quite easy for a drug buyer to withdraw $200 from an ATM to buy heroin or cocaine. Banks don't surveil people who are taking out cash. But it is far more complicated for a drug seller to redeposit that $200. Redeposits are surveiled. To get banknotes back into the system a crook has to launder them, say be sneakily mixing the drug money with legitimate cash earned by

Let's work through how this specific asymmetry has collided with the pandemic. It's unlikely that drug users have stopped buying drugs during the pandemic. (Maybe people are buying even more drugs? Thanks to shut downs, there's not much to do!) So the flow of cash from a drug users' ATMs to a drug dealers' pockets has not slowed at all during the pandemic.

But the network of restaurants and other businesses that drug dealers rely on to launder their funds have all shut down thanks to virus fears and lockdowns. These closures would have put drug dealers, crooks, the mob, etc. in a tough position. Throughout the pandemic they have been accumulating ever more cash from drug using customers, with no place to offload it.

So to sum up, the big increase in cash in the economies of Canada, Europe, US, and the UK is probably being driven by an unwanted accumulation of cash by crooks. Their regular money laundering arrangements aren't functioning.

I don't have any personal experience with being a criminal. But it's fun to speculate about what their lives have been like during the pandemic. The Tony Sopranos, Walter Whites, and Stringer Bells of the world are currently scrambling around for safe places to store their ever burgeoning stores of physical cash. In their houses, at a warehouse storage unit, or at a bank.

And since they can't convert their cash hoards into spendable money in a bank account, I'd imagine these crooks are having problems paying legitimate bills like mortgage payments and the cost of sending their kids to posh schools. With criminal enterprise handling so much extra cash, I'd also imagine that law enforcement agencies are seizing record amounts of cash via civil forfeiture. We could also be seeing a big jump in gang warfare as competing drug outfits raid each other for cash. To recover all of these extra costs of doing business, criminals are probably jacking up drug prices. Yep, I'd imagine it's not an easy time to be a criminal.

As the pandemic subsides and restaurants and other confederate businesses start to open, criminals will be able to restart their money laundering operations. But they won't be able to return their entire accumulated hoard at once. If they were to do so, the cash receipts of the businesses they are using for laundering would stick out, potentially drawing the attention of the tax authority and law enforcement. No, they'll have to slowly reintroduce their dirty money.

Which means the big global jump in banknotes that I illustrated in my first set of charts will take much longer to be worked off than it was accumulated.

PS: I wonder if we can get some other good insights from the data, specifically about the size of the underground economy. Looking at my topmost chart, I'd estimate that the amount of cash in the Canadian economy is about $6 billion higher than it would otherwise be. Let's say that this bulge is entirely due to criminals being unable to launder their drug proceeds. We know Canada has 32 million adults. So Canadians have spent $6 billion on illegal drugs since the pandemic began, or around $200 per adult. That's about $12 billion a year. Seems reasonable, no? (Yes, I am making a load of assumptions here.)